Brett Collett of Equifax shares his perspectives about how finance companies are approaching underwriting in this episode of the Auto Remarketing Podcast recorded during the 2023 Vehicle Finance Conference hosted by the American Financial Services Association.

The vice president of Equifax’s auto vertical also mentioned what other parts of financing are on his radar to watch this year.

To listen to the conversation, click on the link available below.

Download and subscribe to the Auto Remarketing Podcast on iTunes.

Last week was another notable one for industry veteran Daniel Parry.

His company, TruDecision, announced the launch of its credit attribute engine TruDec AE that can integrate application, contract structure, credit bureau and alternative data to provide finance the “next generation” of modeling attributes.

Parry also joined the advisory board for Leasly, a fintech company providing lending, technology and insurance solutions for the automotive industry.

Both operations are relatively new, with TruDecision being one of the first Emerging 8 honorees.

TruDecision’s latest product is calibrated for all credit bureau formats and can allow finance companies to customize their own suite of factors to create predictive models and to control credit policy.

“Today, companies have access to many different modeling forms such as machine learning, logistic regression and support vector machines,” Parry said in a news release from his company. “It does not take much effort for analysts to compare competing models to see which form provides the best results, but this effort is limited by how much predictive power is available in traditional data attributes.

“For years, lenders have been able to acquire thousands of summary variables that are overwhelmingly redundant. To create better models, one must have something new for the algorithms to evaluate. TruDec AE was designed to provide just that,” he continued.

Parry highlighted TruDec AE is the result of more than 25 years of experience as finance companies researching the most predictive factors related to performance, many of which are not represented in the standard off-the-shelf offerings.

TruDecision will be releasing a steady stream of new and enhanced attributes on an ongoing basis. In addition, finance companies will be able to identify their own custom attributes which will be available for their exclusive use, preserving their ability to develop their own competitive advantage.

“In the current environment of increased funding costs, inflation and rising pressure on consumers, it is more important than ever for lenders to drive operational efficiencies,” TruDecision chief revenue officer David Knightly said in the news release.

“The customization feature of TruDec AE allows for increased automation and tighter control over credit policy, as well as performance. Lenders must be able to do more with less, which means scaling without adding substantial headcount,” Knightly went on to say.

TruDecision added that it is in the process of integrating with major loan origination system providers to make the adoption of this innovative system simple and cost-effective.

The company invited finance companies to reach out to TruDecision to learn more about how they can elevate the performance of their business.

Leasly welcomes Parry to advisory board

Leasly is a turnkey new- and used-vehicle leasing solution for dealerships, finance companies and their customers that’s designed to streamline and simplify the front- and back-end vehicle leasing process.

Leasly said its fully automated platform can put significant revenue potential in the dealership’s hands by empowering dealers to lease vehicles in seconds, while providing a convenient and easy-to-use leasing process for consumers.

And the company is looking for Parry to provide additional guidance.

“Daniel Parry is a longstanding and well-respected leader in the finance industry and we’re proud to welcome him to our advisory board,” Leasly CEO Daniel Boller said in another news release. “He brings a proven track record of building analytic platforms to profitably manage credit risk in high growth companies, which is widely recognized in the capital markets.

“I’m confident Daniel’s insights will help us grow the Leasly brand and expand our footprint. Our goal is to put our platform in the hands of more consumers who want a simple and convenient way to lease a car, and more dealers who want a streamlined workflow and a powerful revenue opportunity. I’m pleased Daniel has joined our board and I look forward to his contributions, our collaboration and future growth,” Boller continued.

Parry explained why he decided to become a part of Leasly’s endeavors.

”Daniel Boller, and the rest of the leadership team at Leasly, are top caliber innovators who understand the unique needs of dealers and consumers. They also understand the importance of employing cutting edge risk tools to ensure a top performing portfolio,” Parry said. “I am honored that they reached out to me, and I look forward to helping the company build an outstanding organization.”

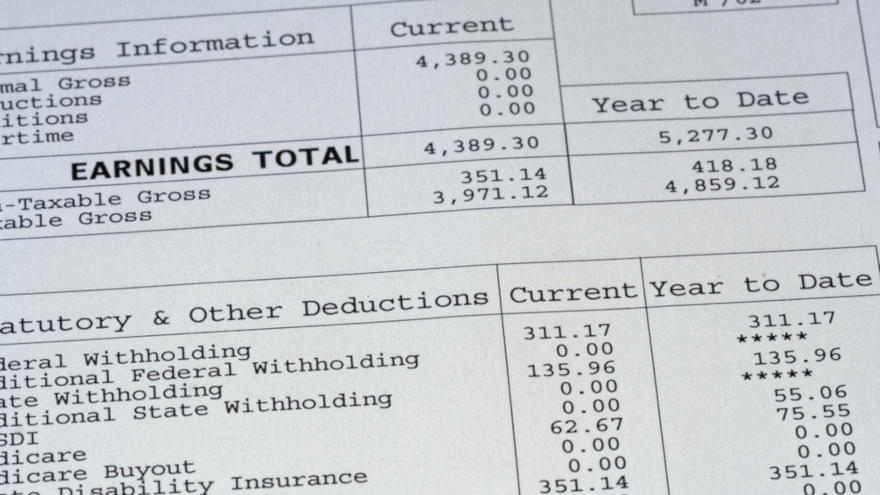

The TurboPass PayStub report rolled out nationally this week.

According to a news release from TurboPass, dealerships in all 50 states now can experience faster funding, more down payments and fraud prevention on customers with payroll data.

Internal TurboPass research has found that more than 2 million people in the U.S. fake paystub documents every year using online resources.

And according to Point Predictive, the number of people falsifying documents to get approved for auto financing has increased 5% year-over-year, jumping to $7.7 billion in 2021.

“When I was running an independent dealership, we had been presented with many fake pay stubs from customers. In the later years, it became increasingly difficult to distinguish between those that were fake and those that were real. It was situations like this that led to the concept for TurboPass,” co-founder and chief operating officer Ken Jarman said.

TurboPass has been helping thousands of dealerships validate proof of employment, income and residence for the last four years, primarily through TurboPass Banking reports. In the last couple of years, dealers have requested over 200,000 banking reports.

Now that the PayStub Report is available, dealers and finance companies will have a tool for verifying W2 income as well.

Like the current TurboPass process, the first step in generating a PayStub report is for the dealer or finance company to send a TurboPass text to the vehicle buyer.

The link included this text message will allow the customer to credential themselves, thereby creating an easy-to-use TurboPass PayStub Report that includes data such as income, employer, job title, start date, employment status, PTI calculations and more.

“It’s been great having another verification tool at the dealership to help speed up and improve the customer experience. It’s made our funding process a lot faster,” stated Greg Skurkovich, dealer principal at URboss Auto, which operates five used-car centers and repair facilities in Illinois, Florida and Pennsylvania. “We require that TurboPass banking or PayStub reports are used on every car deal.”

TurboPass mentioned dealer and finance company partners such as Westlake Financial, Turner Acceptance, and MidAtlantic have tested the product for the last two months with great success, leading the way for other users to follow.

“Dealers, lenders, and consumers are going to experience a frictionless paper-free funding process when using these reports. I’m glad TurboPass is the first to market with their patented point of sale verification process. It’s innovations like this that keep our companies and our industry growing together,” said Kyle Dietrich, senior vice president of acquisitions at Westlake Financial.

Inovatec Systems and TruDecision now are working together for clients in both Canada and the United States.

The provider cloud-based software solutions for finance companies recently announced it has reached an agreement with the developer of artificial intelligence and machine learning-based analytics tools that can improve portfolio performance.

Through this relationship, Inovatec customers will have access to TruDecision’s compelling analytics capabilities through Inovatec’s advanced LOS and LMS platforms, enabling finance companies to automate and improve critical processes like risk mitigation, credit scoring and decisioning, collections and cross-marketing.

Based in Irving, Texas, TruDecision serves a variety of providers, including banks, credit unions, and finance companies. Its solutions are applied in multiple lending sectors, such as automobile, motorcycle, powersports and personal loans.

The company serves lenders in both the United States and Canada and offers customers a unique “analytics-as-a-service” model that can enables clients to use TruDecision on a pay-per-use basis.

“We are always looking to work with ‘best-of-breed’ technology partners that can add significant value to our lenders, especially those innovators that can make an immediate impact in terms of reducing risk and growing the bottom line,” said Bob Metodiev, head of business development for Inovatec. “TruDecision not only ticks the boxes in terms of technology excellence, but also possesses a comprehensive understanding of the challenges and opportunities that define modern lending.

“We are eager to work with the TruDecision team and deliver the compelling analytics capabilities that can have an enormous impact on loan performance,” Metodiev continued.

Inovatec offers cloud-based LOS, LMS and consumer direct technology that can enable finance companies to streamline contract processing, decisioning and management with intelligent automation that can be configured to meet clients’ needs.

The company’s solutions also can allow finance companies to access a variety of innovative services through open APIs, giving lenders the ability to adjust workflows and leverage advanced features like analytics and alternative data to grow their portfolios and build marketshare in a highly competitive industry.

“We are delighted to work with Inovatec, which is not only the established market leader in Canada, but is also rapidly building a sizable customer base in the United States,” TruDecision chief executive officer Daniel Parry said. “We share Inovatec’s belief that every lender-regardless of size or market orientation-should have seamless access to modern analytics capabilities that can have a profound impact on portfolio performance.”

For information on Inovatec’s integrated loan origination system, loan management system, and customer portal solution, visit www.inovatec.com.

LendBuzz co-founder and chief executive officer Amitay Kalmar described the characteristics of artificial intelligence, machine learning and algorithms that intrigue him most during this episode of the Auto Remarketing Podcast.

Then Kalmar explained what those elements now can do for the benefit of underwriting and more within auto finance.

To listen to the conversation, click on the link available below, or visit the Auto Remarketing Podcast page.

Download and subscribe to the Auto Remarketing Podcast on iTunes or on Google Play.

VINData, a provider of trusted vehicle history and remarketing information, recently announced a partnership with Inovatec, a leader in cloud-based loan origination and loan management solutions for the automotive sector.

Through this relationship, VINData will integrate its offerings into Inovatec’s platforms, giving finance companies across the United States and Canada “unprecedented” visibility into the histories of specific inventory to identify potential risks, and improve the management of their collateral portfolios.

The integration into the Inovatec LOS can enable finance companies to seamlessly access VINData information at the time of contract decisioning to quickly and easily evaluate used vehicle collateral risk.

Furthermore, the LMS integration can allows Inovatec clients to monitor the health of their collateral portfolio and identify potential risks before they become financially detrimental.

VINData provides DMV title and brand information, along with data from the National Motor Vehicle Title Information System (NMVTIS) regarding insurance loss and salvage and junk information.

Other data includes active and issued recall data, open liens, active thefts, and vehicle values from leading value guide providers Black Book and NADAGuides/J.D. Power and Manheim Market Report® (MMR).

“We are delighted to work with VINData and provide the company’s vehicle history and associated data to our lenders in a way that makes it easy for them to use,” Inovatec chief executive officer and co-founder of Vlad Kovacevic said in a news release.

“VINData’s highly customizable approach lets us tailor the data to meet specific lender requirements, and we anticipate that the offerings from VINData will be an important source of information to lenders who book multiple vehicle types, both in the U.S. and Canada,” Kovacevic continued.

VINData president Adam Siner added, “Inovatec is exactly the type of integration partner we look for.

“The company’s platform is the perfect conduit to deliver the real-time vehicle history and decisioning information that lenders need to optimize profits and reduce risk. We are very proud to partner with Inovatec and join their efforts to provide world-class services,” Siner went on to say.

On Tuesday, Point Predictive, the San Diego-based company and former Emerging 8 honoree that provides artificial intelligence (AI) solutions to finance, announced a strategic partnership with Provenir, a global leader in AI-powered risk decisioning software for the fintech industry.

Available through the Provenir Marketplace, Point Predictive said its artificial and natural intelligence solutions can provide Provenir customers with increased underwriting automation, simplified data integration and solutions that can enable finance companies to fast-track applications with a low risk of default based on fraud or material misrepresentation.

Furthermore, the small percentage of applications with a high risk of fraud can be flagged for additional investigation, according to a news release.

“Provenir’s cloud-native data, AI and decisioning platform align perfectly with Point Predictive’s AI-based solutions,” Point Predictive chief executive officer Tim Grace said in the news release. “We are confident this partnership will empower Provenir customers to increase efficiency, streamline the lending experience, and be more competitive overall in the dynamic, digital lending marketplace.”

Provenir pointed out the strategic partnership with Point Predictive is growing proof that shared data, insight, and AI is the future of digital transformation in financing and fraud risk mitigation.

“We look forward to working with Point Predictive, a company that shares our philosophy that collaboration and automated decisioning workflows uncover insights that drive businesses forward,” said Carol Hamilton, senior vice president of global solutions at Provenir.

“Point Predictive’s sophisticated, data-based automation and fraud risk mitigation solutions — combined with Provenir’s proven AI-powered decisioning platform — will help customers increase profitability while decreasing risk,” Hamilton went on to say.

Point Predictive director of partnerships Andrew Stamps added these perspectives.

“Point Predictive and Provenir’s solutions complement one another in numerous ways,” Stamps said. “Ultimately, this partnership helps lenders operate faster and with more agility, resulting in greater levels of efficiency and success.”

TurboPass finalized another path for dealerships and finance companies to use its tools for income verification and other parts of the underwriting process.

A couple of weeks after announcing its solutions were available through DealerCenter, TurboPass said that effective Oct. 20, dealers can integrate with RouteOne.

The move means RouteOne dealers are eligible to access the new sharing feature within their TurboPass dashboard.

The new feature can send TurboPass reports directly from the TurboPass dashboard to their RouteOne deal jacket for inclusion in the eContract distribution to finance sources making it easier to experience faster funding, fraud prevention, and reduced finance company fees.

TurboPass reiterated that it can save valuable time in the vehicle buying and closing process.

With the TurboPass dashboard, dealers can send their customer a text to validate the customer’s income and ability to pay in seconds. A unique TurboPass code is generated for each customer, allowing dealers to easily view, print, and submit the customer’s stips in their deal jacket.

To use the new feature in the TurboPass dashboard, the company said users will click the share button next to a completed report and then select the “Share with RouteOne” option. When sharing for the first time, dealers must enter their RouteOne username and RouteOne dealer ID.

After this step, TurboPass will remember these credentials.

Finally, the dealer will click a blue share button which appears to the bottom right of the pop-up, and the report will be instantly added to their RouteOne deal jacket documents.

RouteOne director of OEM strategy and key accounts John Earles explained in a news release from TurboPass what this move can mean for dealer clients of both service providers.

“As an open integration platform, RouteOne is pleased to bring our dealer network the availability of TurboPass integration and the new features it provides,” Earles said. “This integration displays our shared dedication to create a frictionless, modern consumer experience for our dealers and their consumers.”

TurboPass chief executive officer Mike Jarman added, “We’re very pleased to have our dashboard ready for easing sharing with RouteOne. It's a leading platform which provides all the tools necessary for dealers to be successful with their lenders.”

On Tuesday, Digital Matrix Systems and New Orleans-based Crescent Bank highlighted how they’re now working together.

The risk management solution provider announced that Crescent Bank has selected the company’s trended attributes in support of a new and sophisticated modeling approach.

The bank has been providing auto financing and other banking services to consumers across 32 states since 1991.

Digital Matrix Systems explained that the ability to predict consumer behavior at each stage of the customer lifecycle impacts both the management of risk as well as revenue potential. The company noted that a “trended” view of the customer leverages credit data at specified points of time, including credit utilization, past balances, and payment history.

Rather than relying on a credit snapshot from a single point in time, Digital Matrix Systems said trended data points can reveal consumer behavior over extended periods of time and empower better lending decisions.

Does the applicant have the financial discipline to make loan payments as agreed and on time? Digital Matrix Systems pointed out that trended attributes are normalized and can provide insight to that question and others by delivering a history of tradeline balance information.

According to a news release, Crescent Bank will leverage the DMS Summary Attributes in its models to include leveraging trended data. This set of standardized and normalized attributes consolidates credit information for easier analysis by application and decisioning platforms and provides consistency over multiple bureaus and bureau versions.

Executives said that using the trended attributes from DMS will help Crescent Bank maximize insight into consumer behavior in support of effective auto financing decisions.

“Digital Matrix Systems will be a great partner to us as we continue to evolve our modeling approach,” Crescent Bank chief risk officer Benjamin Vega said in the news release. “The DMS trended attributes will provide us with a much clearer view into consumer behavior, which in turn will help us support more customers with their vehicle purchases.”

Digital Matrix Systems vice president of business development Carson York added, “We are thrilled to work with Crescent Bank. We support all of our clients with a similar goal in mind: to help them get the most from their data through analytics that mitigate risk while increasing profitability.

“The DMS Summary Attributes are tri-bureau, which gives Crescent Bank a strong strategic foundation for the future. Our team looks forward to a long and meaningful partnership,” York went on to say.

Complications created by the pandemic made the job of underwriting departments even more challenging since that segment of finance companies is tasked with confirming a myriad of details to ensure quality paper flows into portfolios.

To support the collective recovery of businesses and consumers, Experian this week announced its expansion into employer services and the release of its new suite of real-time income and employment verification products: Experian Verify.

Experian acknowledged the COVID-19 pandemic amplified finance companies’ need for deeper insights into a consumer’s financial situation. At the same time, the credit bureau understood that employers, human resources and tax professionals were flooded with record-breaking unemployment claims, stay-at-home orders, income and employment verification fulfillment requests and more.

“We’re committed to helping employers, businesses, lenders, and consumers on the road to recovery from the pandemic and beyond,” said Alex Lintner, group president of Experian Consumer Information Services. “To support this, we’re building two businesses: Experian Employer Services and Verification Solutions.

“These businesses will create meaningful change and provide our clients with competitive options to achieve their verification needs while helping improve access to credit for consumers,” Linter continued in a news release.

Why the tool is launching now

Experian explained that supplementing information from a consumer’s credit report with income and employment status can create greater opportunities for consumers while helping finance companies extend credit responsibly. Experian Verify is designed to improve borrowing experiences and support consumers with limited credit histories by empowering finance companies to verify income and employment status in real-time.

While verification of income and employment is required in mortgage lending, the practice has become more common across other types of finance since the onset of the pandemic — especially auto.

“The value of verification of income and employment data is evident across the entire credit cycle,” Celent senior banking analyst Craig Focardi said in the Experian news release. “Celent’s perspective on the loan origination market is that borrower situations are changing and all types of retail lenders are competing with each other to attract customers.

“Experian Verify addresses numerous pain points: customer service, cost, and competitive issues facing financial institutions,” Focardi continued.

With Experian Verify, finance companies can create a more complete picture of a consumer’s financial situation quickly and easily.

The products can offer credit card, personal loan, auto finance and mortgage providers as well as tenant screeners and employment screeners with “near-instant access” to tens of millions of active records to verify an applicant’s income and employment status in origination, account review and prequalification decisions.

Powered by Experian’s growing network of payroll and proprietary employer data, the company said finance companies have flexible yet secure access to income and employment records through Experian Verify.

With a consumer’s consent, finance companies can request the information from Experian and an income and employment report can be delivered to providers through an API, online Experian dashboard or paired with an Experian credit report.

Paving the way for industry advancement

Experian highlighted that its recent acquisitions of Corporate Cost Control (CCC), Tax Credit Co. (TCC) and Emptech, as well as its growing network of direct payroll access can deliver “unique and differentiated” employee records into Experian Verify and lay the foundation for the company’s move into employer services.

With all three entities now under one roof, Experian is trying to unlock their collective strength to provide employers, HR, finance and tax professionals with a one-stop-shop to outsource complex and time-consuming tasks more quickly, cost effectively and securely. Services provided by Experian include:

— Employment and income verification

— Electronic I-9 verification management

— Work Opportunity Tax Credits (WOTC) management

— Unemployment claims management

— Other tax credits and incentives

“As we begin to recover from the COVID-19 pandemic and employers are reopening their doors, we’re confident we have assembled the best-of-the-best to help employers overcome their toughest challenges,” said Michele Bodda, president of Experian Mortgage, Employer Services and Verification Solutions.

“We’re committed to leveraging our combined capabilities and focus on high-touch customer service to deliver secure, scalable and transparent services to employers,” Bodda went on to say.

For more information on Experian Verify, visit www.experian.com/verify. To learn more about Experian’s Employer Services business, visit www.experian.com/employer-services.