GWC Warranty wanted to give dealers recommendations to develop new processes designed to increase customer satisfaction and build loyalty.

So this week, the provider and administrator of automotive F&I products released a free eBook titled, “A Dealer’s Guide to Transparency in the Sales and F&I Process.”

“Auto dealers have made great strides towards being more transparent, but there is still a significant gap to fill between dealers’ perceptions and consumer expectations,” said James Virgoe, senior vice president and managing director of GWC Warranty, an APCO Holdings Brand.

“In fact, a recent Capital One survey found that 77% of dealers believe the car buying process is transparent, but only 26% of buyers agree,” Virgoe continued in a news release.

Through the ebook, GWC Warranty highlighted that dealers will learn why transparency is important, the benefits they can see if they deliver more transparency, as well as what information consumers want during the purchase process.

The company added that the eBook shares tips for building a culture of transparency in the dealership and best practices for developing a transparent sales and F&I process.

“The last two years have been an anomaly in auto retailing, where dealers have benefited from high profit margins and PVR,” Virgoe said. “As the market becomes more competitive, dealers will need to deliver a transparent process if they want to attract and retain new customers. Today’s consumers no longer accept a paradigm where they are kept in the dark about pricing and other aspects of the purchase process.”

To download your free version of “A Dealer’s Guide to Transparency in the Sales and F&I Process,” visit the GWC Warranty Resource Library.

Through a recent installment of its tip of the week, Ignite Consulting Partners tackled a strategy that some collections departments might use to kickstart stalled efforts to find and reach their delinquent account holders.

Perhaps the opposite of text messaging, Ignite acknowledging that some collections departments use door knocking to try to physically find the contract holder. Before offering four recommendations if managers want to proceed, Ignite’s compliance experts explained three considerations before embarking on that path.

“Collections is an inherently risky activity and can be compounded by door knocking. In general, Ignite takes the position that in-person door knocking, if not done right, can add additional risk, such as the safety of your customers and employees. There are several things to consider if you are going to use this collections strategy,” the firm said in a recent industry message.

“First, you need to have a robust written policy documenting the purpose of the activity,” Ignite continued. “Second, once you have documented your accepted procedures, you must implement a demonstrable, ongoing training program to ensure employees are adhering to the written processes.

“Third, you need to have an audit function that looks at aspects of the process like success rate and complaints. This audit function should be reviewed in a monthly or quarterly review and used to identify and correct any issues,” the firm went on to say.

At the very least, Ignite said collections departments should consider these four elements when using or implementing a door-knock program:

• Don't lie about who you are or why you are there

• Confirm the identity of the person you are speaking with

• Don't share any information with a third party

• Have a conflict avoidance process

“Other considerations might include your insurance in the instance an employee is injured, or they get in a wreck,” Ignite said. “Does your insurance cover those activities? Are they driving company cars or their own cars? What happens if they get in a wreck conducting company business in their personal vehicle? These are all situations that involve risk for the employee, the customer, and the company.”

Still want to proceed with door knocking? Ignite said managers can discuss strategy in more detail with its firm experts by sending email to [email protected] or calling (817) 928-4303.

Becky Chernek of Chernek Consulting appeared on the Auto Remarketing Podcast for her monthly visit to discuss F&I strategy.

During this episode, Chernek explained why “rehashing the deal” can be a valuable process that can help dealerships, finance companies and consumers.

To listen to the conversation, click on the link available below, or visit the Auto Remarketing Podcast page.

Download and subscribe to the Auto Remarketing Podcast on iTunes or on Google Play.

Nordis Technologies recently unveiled a new white paper that asserted cloud-based customer communications management (CCM) technology enables billing and collections firms to keep up with proliferating rules and requirements for how they are allowed to communicate with consumers about delinquent debt

According to white paper titled, “Gain Control of Your Omnichannel Collections Communications,” another key takeaway is that omnichannel cloud CCM platforms can give accounts receivable management (ARM) companies the control and agility needed to stay compliant and effective in connecting with consumers and increasing recovery.

“We needed the flexibility and ability to react as fast as the industry changes,” Simon’s Agency chief operating officer Tim Buckles said in the white paper. “We also wanted a CCM system that let us take advantage of new digital channels. It’s critical to staying current and relevant.”

Secure and HIPAA-compliant, Nordis Technologies explained that cloud CCM systems can let collectors simplify, expedite and automate development, distribution and updating of print and digital debt communications.

Thanks to its easy-to-use CCM platform, early-out and bad-debt collections leader Meduit implements new letters in 24 to 48 hours and any subsequent edits are made in minutes.

Before moving to a CCM system, Meduit spent 30 to 60 days simply setting up letters with vendors for each new client, according to the white paper.

“In this fast-paced, complicated collections environment, manual processes and slow, costly back-and-forth with letter vendors won’t cut it,” said Bryan Ten Broek, vice president of business development for Nordis Technologies and white paper author.

“To successfully navigate the changing regulatory and business landscape for debt communications, accounts receivable management companies need to leverage CCM software to digitally transform their operations and improve consumer engagement and collections,” Ten Broek continued.

The white paper details how CCM technology delivers significant strategic, operational and financial benefits. In particular, CCM systems can enable collectors to adapt their communications more quickly to meet regulatory and legal requirements governing debt collection letters and communications.

Additionally, using programmed business rules, Nordis Technologies mentioned ARM firms can automatically include only the disclosures that each recipient needs, based on such parameters as state, ZIP code, and communication type, including the Reg F safe harbor letter for debt validation notices.

Nordis Technologies added that CCM technology also can enables ARM firms to cater to growing consumer preferences for digital communications.

“Using preferred contact and communication methods increases the likelihood of getting paid. Right now, the recommended payment method by the CFPB is check. The average millennial uses almost any method of payment other than check,” Buckles said.

For more information on digitally transforming debt communications to drive consumer engagement and higher collections, you can download the white paper via this website.

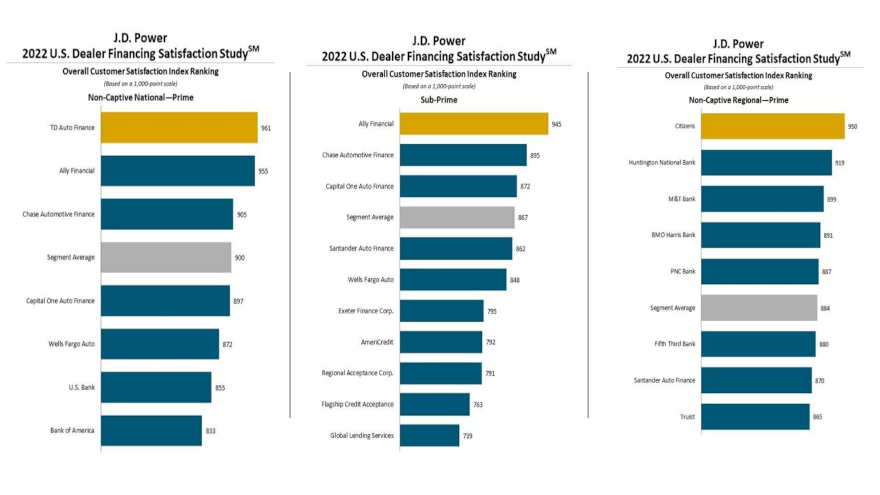

Ally Financial topped the ranking among subprime auto finance companies for the second consecutive year, according to the J.D. Power 2022 U.S. Dealer Financing Satisfaction Study, which was released on Thursday.

Ally Financial ranked highest in overall dealer satisfaction among finance companies that participate in the subprime market with a score of 945 on a 1,000-point scale. Chase Automotive Finance placed second at 895, and Capital One Auto Finance came in third at 872.

J.D. Power highlighted that Ally Financial also ranked highest in overall dealer satisfaction in the leasing space, compiling a score of 942. That performance was followed by Subaru Motors Finance (940) and Ford Credit (906).

In the captive mass market segment, Subaru Motors Finance took first place in overall dealer satisfaction with a score of 934, followed by Honda Financial Services (899) and Ford Credit (888).

Among non-captive national finance companies specializing in prime paper, J.D. Power reported that TD Auto Finance ranked highest in overall dealer satisfaction for a second consecutive year, with a score of 961. Ally Financial placed second at 955 with Chase Automotive Finance coming in third at 905.

And among non-captive regional finance companies in the prime segment, J.D. Power pointed out that the same company led the way for the second straight year, as Citizens registered the highest score for dealer satisfaction at 950. Huntington National Bank landed in second at 919 with M&T Bank placing third at 899.

Looking how those auto finance providers generated those performances, J.D. Power explained that company sales representatives are facing a challenging marketplace as a combination of inflation, rising interest rates and persistently low supply of new vehicles have made it harder than ever to win new business.

In the full report that available to J.D. Power clients, the company identified five key sales rep behaviors that can mean the difference between winning over dealers with above-and-beyond service or disappearing into the background.

“Auto lender sales reps that exceed dealer expectations in areas such as responsiveness and expertise with lending programs generate dealer satisfaction scores that are as much as 190 points higher — on a 1,000-point scale — than those who just meet or miss dealer expectations,” J.D. Power director of automotive finance intelligence Patrick Roosenberg said in a news release. “Despite this huge competitive advantage, only 44% of sales reps manage to exceed dealer expectations.”

Additionally, Roosenberg noted that banks significantly improved year-over-year and outperformed captives in overall dealer satisfaction.

“Banks have made great strides by focusing on improving dealer satisfaction which leads to greater dealer intent to send more business,” he said.

AUL Corp. senior vice president of sales and marketing Paul McCarthy identified nine F&I tips and trends he sees being in play for dealerships for remainder of the year.

McCarthy touched on topics such as what’s on the dealership website to how much profit stores can expect to generate each time a vehicle is delivered.

Here are those nine thoughts:

1. The future of F&I is bright

With F&I comprising a growing percentage of automotive profits, the future of F&I continues to be very bright. The costs of new and used vehicles are at historic highs and consumers are increasingly looking for ways to protect their investment. In fact, dealers today should have a PVR between $1,500 and $2,000 or greater. If not, it’s time to review your F&I strategy.

2. Role of F&I technology

While new technologies have been a tremendous help in facilitating F&I transactions, especially during the pandemic lockdowns, technology itself is not a final solution. Technology’s biggest impact has been with the process, not the product. The key ingredient to maximizing F&I success is the power of the connection between the finance manager and the customer.

3. Where the future growth of F&I will come

We see F&I growth opportunities coming from high mileage used cars, Hybrid and BEVs, and in the policies that cover the many technological systems found in modern cars. The electrification of the American automotive market is just beginning, and consumers are holding onto their cars longer than ever before, driving up the need for policies that cover vehicles that were previously uncoverable.

4. CPO programs will become increasingly important, even with switch to BEV

Even with the switch to BEVs, we believe CPO programs will become an important avenue for revenue growth. Seventy percent of claims are now non-powertrain components and consumers will need F&I products to cover the rest of the vehicle. And with the cost of parts increasing 30-60% in the last 12 months, coverage is ever more important.

5. Transparency is your key to success in F&I transactions

Studies have shown that the earlier F&I options are introduced to the buyer, whether via the website or during the sales process, the more likely they are to be purchased. We recommend dealers allow the customer to review all their F&I options from the outset of the relationship. The greater the transparency, the greater the results.

6. F&I will continue to be a driving force in dealer profits

Not only are F&I policies more popular than ever with consumers, chargebacks have seen decreases as much as 90% in the last 24 months. Today’s customer understands why they purchased their specific policies and are far less likely to cancel. And proper F&I disclosure creates a desire to purchase and maintain coverage.

7. F&I revenue sharing for dealers will continue to increase

While dealers are making increased profits from F&I at the time of the sale, F&I revenue sharing provides a further opportunity to realize revenue for the life of each policy. F&I sales are accomplished through a unique, collaborative partnership between insurer, agent and dealer, and as the final dealmaker in the process, it is a natural progression for dealers to have an opportunity to share in the long-term revenue.

8. The talent and skill of the F&I manager and the agent are what will drive PVR growth.

While new technology speeds and improves the sales process, and full transaction transparency increases your efficiency, it is the talent and skill of your F&I manager and agent that will drive your PVR growth. We believe that behind every great finance manager is a great agent; one who can provide the proper tools, processes, and training for the whole dealership.

9. Know your dealership

To maximize your F&I sales, know your dealership. Where is the F&I process being started in your dealership — on the website, at the sales desk, showroom floor, F&I office? Ideally, it should begin as soon as possible. If feasible, add F&I options to the website. If adding to the website is not an option, introduce the menu at the sales desk or showroom floor. Studies have shown the earlier you introduce F&I options, the more likely the customer is to purchase.

One of the leading F&I consultants agreed to begin a new monthly series as part of the Auto Remarketing Podcast.

Becky Chernek opened the series by giving her perspectives on what’s changed in the finance office since the pandemic arrived as well as her No. 1 recommendation that she has provided clients as a result.

To listen to the conversation, click on the link available below, or visit the Auto Remarketing Podcast page.

Download and subscribe to the Auto Remarketing Podcast on iTunes or on Google Play.

Daniel Parry did not seek to have an economic or political argument about whether the U.S. is officially in a recession. Rather, the co-founder and chief executive officer of TruDecision maintained that risk is in play no matter how well the economy may or may not be doing.

Parry pointed out more than a half dozen data points that company decisionmakers could watch to make informed choices. Then, Parry shared a trio of recommendations he’s offered to other clients of his fintech company that’s focused on bringing competitive advantages to finance companies through analytic technology.

He introduced his commentary shared online via LinkedIn this way.

“You cannot turn on the news these days without hearing hostile arguments about whether we are or are not already in a recession,” Parry wrote. “With news of a second consecutive quarter of GDP decline, those who dislike the current administration declare that we are. Those on the other side of the aisle say that two consecutive quarters of decline is not the official definition of a recession. The latter point to various economics professors and the National Bureau of Economic Research (NBER), which sets the official dates of economic cycles.”

Parry then asserted, “My answer to this debate is ‘who cares?’”

What Parry thinks what finance companies should care about include metrics such as unemployment, consumer sentiment, the ISM Manufacturing and Services Index, the inverted yield curve, inflation and interest rates.

After examining those trends, Parry recommended three strategies to finance companies, beginning with ensuring it has excess debt capacity.

“It is wise to retain debt capacity so as to continue funding loans, particularly if the securitization market contracts or becomes impractically expensive,” Parry wrote.

Next, the TruDecision leader mentioned that finance companies can consider modifying requirements for the maximum amount financed and minimum down payment.

“Modest changes can go a long way to leveling off performance volatility across the credit cycle,” he wrote.

Finally, Parry urged finance companies to watch wholesale vehicle values.

“As vehicle values decline, which is likely over the next 18 to 24 months, it will be increasingly important for credit managers to slowly offset those declines with tighter policy in the lowest tiers,” he wrote.

If you have more questions, you can reach Parry at [email protected].

Ignite Consulting Partners directed one of its recent tips of the week at collection departments and their staff. When touching on third parties and references, Ignite asked the question many collectors might, too. “What can you say and not say?”

Firm experts responded to that question by stating, “Don’t be a victim of bad habits and information.”

They continued by acknowledging many collectors “just naturally assume that if a customer isn’t communicating it’s acceptable to start calling references and other third parties. It’s not and it can create liability.

“The general rule is that references and other third parties can be contacted to learn the location or good contact information of the account holder. If you are in contact with the account holder, then you don’t need to speak to a third party, and doing so can create liability,” Ignite went on to say.

The firm suggested that finance companies and their collections departments document account notes about why contact with a third party is needed. The reasons could be the customer is “lost,” has changed a phone number or direct mail has been returned.

“These facts can be important later,” Ignite said.

Experts wrapped up this skip-tracing discussion with these points.

“If contact with a third party is appropriate, then be sure to understand the limits,” Ignite said. “The collector can identify themselves and say they are trying to locate the customer and the third party was provided as a reference. If asked, they can say whom they work for. They should never discuss the account status, the underlying debt, or any other information.

“There’s lots of litigation on this subject, both from customers and third parties, so make sure your team knows the rules,” the firm went on to say.

If you would like to discuss your insurance policy, or just want to talk about your situation, you can contact the compliance professionals at Ignite Consulting Partners via email at [email protected] or call directly at (817) 900-8754.

Dealerships and finance companies currently might be encountering unique circumstances, but EFG Companies recommends that they approach the current automotive retail and financing landscapes with a strategy that’s likely worked for decades.

The provider of consumer protection programs for vehicles said through a news release that it sees several market opportunities in the second half of year for the retail automotive, powersports, and F&I industries. But EFG Companies recommends caution due to market volatility, continued supply chain and product inventory issues and challenges to consumer financial strength.

Company leaders also suggest that dealer principals, agents and finance companies approach the remainder of the year strategically focused on implementing customer-first sales methods, optimizing inventory with value-driven products, and implementing training to ensure employee effectiveness and regulatory compliance.

“While there are many factors at play, smart business owners will stay strategically focused on those tasks which align with the needs of consumers while advancing their businesses in post-COVID sales models,” EFG Companies chief revenue officer Eric Fifield said in the news release.

“The new normal is now, and consumers have clearly shown how they want to do business. Regardless of how economic factors play out, there remain numerous opportunities for revenue in the remainder of 2022,” continued Fifield, who elaborated more about the current market in this online video.

Fifield and other executives from EFG Companies emphasized that consumers continue to look for added value in their automotive and powersports purchases. They explained this various segments this way:

Embracing new approaches to drive revenue growth for retail automotive dealers

EFG companies said post-COVID strong consumer financial positions, favorable credit terms and pent-up demand all spell revenue opportunities for dealer principals in the second half of 2022.

“Dealers who embrace new selling models, train and support their sales teams, and are mindful of regulatory scrutiny will capture the sale versus others who pine for the return of the old days,” executives said.

Growth in off-road, personal watercraft sales equals opportunities for powersports dealers

EFG Companies pointed out that consumers are anxious for adventure, and dealers with off-road or personal watercraft units who have successfully implemented online sales models with supporting F&I products and suitable margins will fare better than businesses who focus solely on front-end gross.

Agents making vehicles more marketable can deliver win-win opportunities

EFG Companies said agents will need to “flex different muscles” to provide heavier engagement as dealers adjust their operations for continued growth.

“Those with the right focus and service offering to help tackle current dealership challenges will be better positioned to generate more dealership revenue, attract new clients, and boost service retention business across the board,” executives said.

Finance companies delivering greater protection should produce greater value

EFG Companies emphasized that customer-focused finance companies can capture valuable auto paper through affordable protection products that retain vehicle value while differentiating themselves.

“While economic uncertainty persists, and unpredictable supply chain and inventory challenges could introduce added volatility, dealers, agents, and lenders who strategically focus on meeting customer needs while maximizing employee effectiveness will be best positioned for a profitable 2022,” executives said.