Equifax recently made two moves in an effort to make select differentiated data assets more widely available.

Equifax announced one offering through AWS Data Exchange through Amazon Web Services (AWS) and another through the Snowflake Data Marketplace.

The path through AWS can allow users to find, subscribe and use third-party data in the cloud. This relationship builds on the Equifax Cloud strategy and makes anonymized Equifax Analytic Dataset consumer and loan-level credit data, U.S. Consumer Credit Trends macro-level information, B2bConnect commercial marketing data, IXI economic data and unique property and housing data quickly and easily available to business customers for improved decision intelligence.

“Equifax understands that smarter data insights drive smarter actions,” said Joy Wilder Lybeer, United States Information Solutions (USIS) chief revenue officer and senior vice president of global Partnerships at Equifax.

“AWS Data Exchange gives our business customers secure and efficient access to our differentiated data offerings,” Wilder Lybeer continued in the first of two news releases from Equifax. “This allows them to more quickly access the insights they need to drive smarter revenue and create better customer experiences with the speed and security of the cloud.”

Equifax recapped that it invested $1.5 billion in its enterprise-wide infrastructure, which is specifically tailored to highly regulated data workloads. The Equifax Cloud is the foundation of the Equifax business and can allow seamless, secure delivery of data assets to AWS Data Exchange for customers to easily leverage within their broader AWS workloads.

“Equifax has reimagined and reengineered our tools, technology, and assets in the cloud for optimal performance and customer benefit,” said Mark Luber, chief product officer for Equifax USIS.

“Making select Equifax credit, marketing and economic datasets available through the AWS Data Exchange underscores our commitment to our customers, bringing the decision intelligence they need to optimize growth and better serve their own customers,” Luber added.

Meanwhile, in connection with the partnership with Snowflake, the relationship also is designed to make select differentiated data assets rapidly and securely available Snowflake Data Marketplace through a frictionless data sharing experience with no data transfer or integration requirements.

It’s all tailored to enable data scientists, business intelligence and analytics professionals access to live and ready-to-query data from Equifax for smarter decision making.

Like with AWS, customers now can leverage Snowflake’s Data Cloud to rapidly obtain anonymized Equifax Analytic Dataset consumer and loan-level credit data, U.S. Consumer Credit Trends macro-level information, B2bConnect commercial marketing data, IXI economic data and unique property and housing data for new decision intelligence.

“Equifax understands that to be successful and to achieve repeatable, profitable and sustainable business growth, our customers need to be able to make predictive and informed decisions quickly,” Wilder Lybeer said in the other news release.

“By bringing our unique data to Snowflake Data Marketplace, we’re meeting organizations with the insights they need through their channels of choice — making critical insights more easily available to more customers in a highly secure environment. “

Equifax participation in Snowflake Data Marketplace also is enabled by the Equifax Cloud.

“Equifax and Snowflake share the understanding that more data enables better decisions,” said Matt Glickman, vice president of customer product strategy, financial services, at Snowflake.

“Snowflake Data Marketplace is designed to deliver data at scale in the Data Cloud without compromising data privacy and security. Inclusion of Equifax datasets supports Snowflake customer demand for differentiated data across industries that drives decision intelligence,” Glickman went on to say in the news release.

A potential pitfall of digital retailing recently impacted a luxury automaker.

And it might have stemmed from activity long before the pandemic arrived and pushed automakers and dealerships deep into the digital domain.

According to a news release, a vendor informed Mercedes-Benz on June 11 that sensitive personal information of less than 1,000 OEM customers and interested buyers was inadvertently made accessible on a cloud storage platform.

The automaker said this confirmation was part of an ongoing investigation conducted in cooperation with the vendor.

Officials indicated the issue was uncovered through the “dedicated work” of an external security researcher. They said it’s their understanding the information was entered by customers and interested buyers on dealer and Mercedes-Benz websites between Jan. 1, 2014 and June 19, 2017.

“No Mercedes-Benz system was compromised as a result of this incident, and at this time, we have no evidence that any Mercedes-Benz files were maliciously misused,” the automaker said in the news release.

“Data security is a serious matter for MBUSA. Our vendor confirmed that the issue is corrected and that such an event cannot be replicated. We will continue our investigation to ensure that this situation is properly addressed,” the OEM continued.

Mercedes-Benz also shared that the vendor reports that the personal information for these individuals — again evidently less than 1,000 according to the OEM — is comprised mainly of self-reported credit scores as well as a very small number of driver license numbers, Social Security Mumbers, credit card information and dates of birth.

“To view the information, one would need knowledge of special software programs and tools — an Internet search would not return any information contained in these files,” the automaker said.

The OEM went on to note the investigation was initiated to assess the accessibility of approximately 1.6 million unique records. The company indicated the vast majority of these records included information such as name, address, emails, phone numbers and some purchased vehicle information.

“However, MBUSA would like to stress that a review of the total data entry record set determined that less than 1,000 individual Mercedes-Benz customers and interested buyers had additional personal information in a publicly accessible state,” the company said.

“Mercedes-Benz USA has already begun notifying individuals, whose additional information was accessible, about this incident,” the company went on to say.

The automaker added that any individual who had credit card information, a driver’s license number or a Social Security Number included in the data will be offered a complimentary 24-month subscription to a credit monitoring service.

“We will also notify the appropriate government agencies,” officials said.

Any individuals who have questions or concerns about this incident can contact the Mercedes-Benz Customer Assistance Center at (800) 367-6372.

Twelve months — and counting — through a pandemic era has done far more than simply disrupt normal business operations for the automotive industry. As a result, various stakeholders are revisiting fundamental assumptions that have been in place for years. The stress caused by uncertainty in the market has created a demand for a new level of transparency — driven by digital channels of engagement. This trend is structurally changing relationships among lenders, dealerships and consumers.

Moving deeper into 2021, we expect to see continued challenges in the automotive industry including inventory shortages in both new and used vehicles, as well as supply chain disruptions. Lenders will have to access the best, most accurate and current information to achieve important business objectives. Analyzing the changing risk landscape to make smart decisions about loan portfolios will emerge as an important competitive factor among lenders in the months and years to come.

Higher quality data available

For many years, lenders relied on standard VIN decoders which offer partial—and sometimes incorrect—data about vehicle features and packages. In many cases, these limitations led to imprecise valuations for specific vehicles and resulted in costly oversights and missed opportunities. In the salad days leading up to March of 2020, a highly profitable market could absorb these inefficiencies. The situation today, however, is different.

Today, two major developments are unfolding:

1. A significant evolution in industry relationships across the value chain is making more data available to the automotive community of interest

2. Dramatic developments in technologies — such as artificial intelligence, machine learning and big data analytics — that capture insights from disparate sources.

These two trends inspired J.D. Power to make significant investments in its data-gathering and analytical capabilities, which have manifested themselves with the addition of ALG and ChromeData to the J.D. Power family. The increased amount of data and advanced analytical tools leveraging AI technologies have resulted in a new J.D. Power offering called VIN Precision+.

VIN Precision+ unlocks the full 17-digit VIN code and erases blind spots associated with traditional VIN decoding. This solution is a robust and intelligent resource that vastly improves lenders’ ability to engage in:

• Risk mitigation: Lenders can now know beyond all reasonable doubt that they are lending the right amount of money based on a detailed understanding of the features and content associated with vehicles they are underwriting.

• Portfolio valuation: As individual loans become part of the broader portfolio under management it is imperative that they can optimize capital allocations.

• Repositioning and remarketing: As vehicles in the portfolio complete their lifecycle and return to the aftermarket for auction, they can ensure that their assets are valued correctly.

Better data equals better profitability

VIN Precision+ is having a significant — and positive — effect on portfolio valuations. It has provided lenders with the edge they need to weather future disruptions that are expected to emerge in the market — especially as forbearance programs and other economic activities expire. Two real-world scenarios that demonstrate how important accurate data is for lenders include:

• Vehicle Audits: J.D. Power compared a portfolio analysis using standard VIN decoding to VIN Precision+ results for a lender with a portfolio of approximately 500,000 vehicles. The standard VIN decoding estimated that portfolio to have a value of $10.3 billion. The more granular VIN Precision+ analysis revealed a 1.8% difference in the portfolio valuation. This resulted in a $180 million discrepancy. This is not an insignificant number for a sector with tight margins in which every percentage point counts.

• Future-Proofing Loan Practices: Lenders using standard VIN decoding practices often receive inaccurate — or incomplete — information on a specific vehicle’s package and trim options. In an experiment with a lender, a vehicle was randomly selected for a J.D. Power audit using VIN Precision+. The lender had valued the vehicle at approximately $40,000. The VIN Precision+ analysis revealed that it was only worth $35,000. Replicated, this inaccuracy would have a significant negative effect on the overall portfolio value. In this case, the portfolio was valued at $15 million less than the lender had originally calculated.

The ability to capture and analyze granular data offers lenders an opportunity to run their business with a much higher level of confidence — and profitability.

Leland Brewer is director of vehicle valuations at J.D. Power.

Perhaps now Equifax, along with federal and state regulators, can close the chapter of the company’s history that included the 2017 data breach.

On Monday, the credit bureau announced a comprehensive $671 million resolution that includes settlement agreements that would resolve the multi-district consumer class action litigation, as well as investigations by the Federal Trade Commission, the Consumer Financial Protection Bureau, the attorneys general of 48 states, Puerto Rico and the District of Columbia and the New York Department of Financial Services (NYDFS).

If approved by the court, a consumer restitution fund of up to $425 million will be available to pay for three-bureau credit monitoring for consumers whose information was impacted in the 2017 breach, actual out-of-pocket losses related to the breach, and other consumer benefits such as identity restoration services.

Equifax said it has been providing free credit monitoring services to consumers since September 2017.

“This comprehensive settlement is a positive step for U.S. consumers and Equifax as we move forward from the 2017 cybersecurity incident and focus on our transformation investments in technology and security as a leading data, analytics, and technology company,” Equifax chief executive officer Mark Begor said.

“The consumer fund of up to $425 million that we are announcing today reinforces our commitment to putting consumers first and safeguarding their data — and reflects the seriousness with which we take this matter,” Begor continued. “We have been committed to resolving this issue for consumers and have the financial capacity to manage the settlement while continuing our $1.25 billion EFX2020 technology and security investment program. We are focused on the future of Equifax and returning to market leadership and growth.”

In September of 2017, Equifax announced that a data breach at the company resulted in the exposure of approximately 147 million U.S. consumers’ sensitive personal information, including names, addresses, Social Security Numbers and dates of birth. The bureau coordinated its investigation with the FTC and attorneys general from across the country.

In total, the settlements with these entities would impose up to $700 million in relief and penalties.

Investigation and breach details

The FTC alleged that Equifax failed to patch its network after being alerted in March 2017 to a critical security vulnerability affecting its ACIS database, which handles inquiries from consumers about their personal credit data. Even though Equifax’s security team ordered that each of the company’s vulnerable systems be patched within 48 hours after receiving the alert, the FTC said Equifax did not follow up to ensure the order was carried out by the responsible employees.

In fact, the FTC said Equifax did not discover that its ACIS database was unpatched until July 2017, when its security team detected suspicious traffic on its network. The regulator recapped that a company investigation revealed that multiple hackers were able to exploit the ACIS vulnerability to gain entry to Equifax’s network, where they accessed an unsecured file that included administrative credentials stored in plain text. These credentials allowed the hackers to gain access to vast amounts of consumers’ personally identifiable information and to operate undetected on Equifax’s network for months.

The hackers targeted Social Security numbers, dates of birth, and other sensitive information, mostly from consumers who had purchased products from Equifax such as credit scores, credit monitoring, or identity theft prevention services. For example, hackers stole at least 147 million names and dates of birth, 145.5 million Social Security numbers, and 209,000 payment card numbers and expiration dates.

Hackers were able to access a “staggering” amount of data because Equifax failed to implement basic security measures, according to the complaint. This includes failing to implement a policy to ensure that security vulnerabilities were patched; failing to segment its database servers to block access to other parts of the network once one database was breached; and failing to install robust intrusion detection protections for its legacy databases.

In addition, the FTC also alleges that Equifax stored network credentials and passwords, as well as Social Security numbers and other sensitive consumer information, in plain text.

Despite its failure to implement basic security measures, Equifax’s privacy policy at the time stated that it limited access to consumers’ personal information and implemented “reasonable physical, technical and procedural safeguards” to protect consumer data.

The FTC also alleged that Equifax violated the FTC Act’s prohibition against unfair and deceptive practices and the Gramm-Leach-Bliley Act’s Safeguards Rule, which requires financial institutions to develop, implement and maintain a comprehensive information security program to protect the security, confidentiality, and integrity of customer information.

“Companies that profit from personal information have an extra responsibility to protect and secure that data,” FTC chairman Joe Simons said in a news release. “Equifax failed to take basic steps that may have prevented the breach that affected approximately 147 million consumers.

“This settlement requires that the company take steps to improve its data security going forward, and will ensure that consumers harmed by this breach can receive help protecting themselves from identity theft and fraud,” Simons said.

More information about the settlement

According to a news release from the CFPB, the bureau alleged in its complaint that Equifax violated the law in several ways through its conduct both before and after the breach. Specifically, the bureau alleged, Equifax engaged in unfair and deceptive practices in violation of the Consumer Financial Protection Act of 2010 by:

— Failing to provide reasonable security for the massive quantities of sensitive personal information stored within its computer network, causing substantial injury to consumers whose data was stolen

— Deceiving consumers about the strength of its data security program in its privacy policies

— Engaging in acts and practices that caused additional harm or risk of harm to consumers in response to the breach.

To provide relief for consumers affected by the breach, the bureau’s proposed order requires Equifax to establish a consumer fund with up to $425 million available to provide affected consumers with a broad array of redress. The consumer fund would be used to provide reimbursements to affected consumers for time and money they spent related to the breach.

If the court approves the settlement, affected consumers may be eligible to receive money by filing one or more claims of up to $20,000 per individual for lost time and money for the following:

— $25 per hour for up to 20 hours for time spent protecting personal information or addressing identity theft after the breach

— Money spent purchasing credit monitoring or identity theft protection after the breach

— The cost of freezing or unfreezing credit reports at any consumer reporting agency after the breach

— Reimbursement for up to 25% of the amount paid to Equifax for credit or identity monitoring subscription products between Sept. 7, 2016 and Sept. 7, 2017

— Any unreimbursed costs, expenses, losses, or charges incurred as a result of identity theft

— Miscellaneous expenses associated with any of the above, such as notary, fax, postage, mileage and telephone charges

The CFPB said all affected consumers would be eligible to receive at least 10 years of free credit monitoring, at least seven years of free identity-restoration services, and, starting on Dec. 31, and extending seven years, all U.S. consumers may request up to six free copies of their Equifax credit report during any 12-month period.

These free copies will be provided to requesting consumers in addition to any free reports to which they are entitled under federal law, according to officials

If consumers choose not to enroll in the free credit monitoring product available through the settlement, the bureau indicated they may seek up to $125 as a reimbursement for the cost of a credit-monitoring product of their choice.

The CFPB noted a settlement administrator will manage the claims process. Consumers must submit a claim in order to receive free credit monitoring or cash reimbursements. After the court approves the settlement, consumers can submit a claim online at www.EquifaxBreachSettlement.com, or by mail. Consumers may visit this website to learn about the deadlines for filing claims.

In addition to consumer relief, Equifax would be required to pay the bureau a $100 million civil money penalty. Equifax also would be required to make significant improvements to its data security practices and would be subject to ongoing oversight by regulators.

“Today’s announcement is not the end of our efforts to make sure consumers’ sensitive personal information is safe and secure,” CFPB director Kathleen Kraninger said.

“The incident at Equifax underscores the evolving cybersecurity threats confronting both private and government computer systems and actions they must take to shield the personal information of consumers,” Kraninger continued. “Too much is at stake for the financial security of the American people to make these protections anything less than a top priority.”

New York heavily involved on state level

New York attorney general Letitia James co-led the coalition of 50 attorneys general in reaching the settlement with Equifax.

“Equifax put profits over privacy and greed over people, and must be held accountable to the millions of people they put at risk,” James said in a news release. “This company’s ineptitude, negligence, and lax security standards endangered the identities of half the U.S. population.

“Now it’s time for the company to do what’s right and not only pay restitution to the millions of victims of their data breach, but also provide every American who had their highly sensitive information accessed with the tools they need to battle identity theft in the future,” James continued.

Additionally, the New York State Department of Financial Services (DFS) separately investigated Equifax’s security practices, and found that the company engaged in practices that violated the Dodd-Frank Act and Financial Services Law 408. As a result, Equifax will be fined an additional $10 million by DFS, bringing the total New York State will receive in fines to more than $19.2 million.

“First and foremost, the settlement announced today holds Equifax accountable for its egregious breach in its duty to consumers in safeguarding their sensitive personal identifying information and restores some peace of mind and protection to New Yorkers,” DFS superintendent Linda Lacewell said.

“Strengthening consumer protections for New Yorkers, DFS now requires credit rating agencies to be licensed and supervised by DFS, and comply with the Department’s landmark cybersecurity regulation to better guard against potential breaches,” Lacewell went on to say.

Some consumer advocates still not happy

U.S. PIRG said the “Equifax penalty is a sweetheart deal that leaves consumers at risk.” U.S. PIRG is the federation of state public interest research groups, which are non-profit, non-partisan public interest advocacy organizations.

“Equifax appears to have made a calculated decision that losing the Social Security Numbers and birth dates of some 148 million consumers to identity thieves was worth only about $700 million or a little less,” U.S. PIRG federal consumer program director Ed Mierzwinski said in a news release distributed late on Friday. “The shelf life of financial DNA is forever so this sounds like a sweetheart deal for a company that failed to do its basic job: protect consumer data.

“Failure to protect privacy has a real harm; we think Equifax should have paid real money, not ‘just go-away’ money, and promised real changes to its sloppy last-century practices,” Mierzwinski continued.

Equifax is sharing in hopes of cultivating technological innovation.

The global data, analytics and technology company recently announced a joint collaboration with FinTech Sandbox to help drive global fintech innovation. Equifax highlighted that startups can now leverage various forms of consumer and commercial data from the company in an effort to help these new businesses develop products for the benefit of the industry and consumers.

Nonprofit FinTech Sandbox promotes innovation in the financial sector by making data and infrastructure available to well-qualified fintech startups. In return, Sandbox startups collaborate with current and past residents by sharing learnings and advancements with respect to the fintech ecosystem.

Participating startups pay no fees, and no equity is taken, according to a news release from Equifax.

In addition to data, Equifax said it will give analytical support to the Sandbox by allowing access to its Ignite portfolio of data and advanced analytics solutions. The portfolio can securely and comprehensively support the full analytical lifecycle — from data access and transparency to visualization and deployment — using a single, connected suite of advanced analytics processes, technology and tools.

“The fintech industry is moving fast, and I’m so proud that we have an opportunity to collaborate around our shared mission for advancing the industry. We look forward to helping influence the Sandbox’s next generation of leaders with our data and analytical tools,” said Sharla Godbehere, atlfi and fintech leader at Equifax.

“We’re also offering our expertise in this space,” Godbehere continued. “Being a fintech company, we understand the challenges of bringing all the pieces together to make a product work. This is an exciting opportunity to partner and share our personal insights and experience with these startups.”

Equifax has earned a spot on the IDC FinTech Rankings list consecutively for the past 15 years since it has been produced. It is one of the most comprehensive vendor ranking within the financial services industry.

“At FinTech Sandbox, we have been looking to expand our offerings and support to startups focused on consumer financial wellness,” FinTech Sandbox executive director Jean Donnelly said.

“Equifax, with records for more than 850 million consumers and 92 million businesses worldwide, and advanced analytic solutions, can provide a needed lift for these companies bringing essential solutions to market,” Donnelly went on to say.

As the company gears up to host FICO Auto Mastermind 2019 this week, Nick shared his conversations with a pair of FICO experts who were in San Francisco earlier this year for the Vehicle Finance Conference hosted by the American Financial Services Association.

FICO chief analytic officer Scott Zoldi described what clean data really is as FICO vice president of security solutions Doug Clare revisited the ongoing challenge of maintaining cybersecurity.

The full episode can be found below.

Download and subscribe to the Auto Remarketing Podcast on iTunes or on Google Play.

You can also listen to the latest episode in the window below.

Catch the latest episodes on the Auto Remarketing Podcast homepage and on our Soundcloud page.

Please complete our audience survey; we appreciate your feedback.

NACHA highlighted the ACH Network, an electronic payment system that safely and reliably moves tens of billions of payments annually, generated another milestone in 2018.

Officials indicated payment volume climbed by almost 1.5 billion payments, marking the fourth straight year the ACH Network has added more than 1 billion new payments.

NACHA said the ACH Network volume reached nearly 23 billion payments in 2018, a year-over-year increase of 6.9 percent and the highest growth rate since 2008. That’s nearly 70 payments for every person in the U.S.

The value of ACH payments in 2018 was $51.2 trillion, a 9.5-percent increase over 2017. It marked the sixth consecutive year in which the ACH payment value has risen by at least $1 trillion. For perspective, the value of last year’s ACH payments was more than two-and-a-half times that of the nation’s 2017 gross domestic product.

Officials went on to mention same-day ACH volume soared in 2018, the first full year with same-day debits as well as credits. There were nearly 178 million same-day ACH payments last year: 98.3 million credits and 79.7 million debits.

Overall, same-day ACH volume jumped 137 percent from 2017. Total same-day ACH value in 2018 was $159.9 billion, up 83 percent over the previous year.

“The results for 2018 make clear that the ACH Network is vibrant and continues to be a vital component of the nation’s economic engine,” NACHA chief operating officer Jane Larimer said.

“With more enhancements to same-day ACH being rolled out this year and next, the experience for businesses and consumers will only get better,” Larimer continued.

NACHA noted several core ACH use cases saw substantial growth in 2018 including:

• Business-to-business (B2B) payments rose 9.4 percent to 3.6 billion with a total value of $34.9 trillion.

• Direct deposits climbed 4.4 percent to 6.8 billion for total value of $9.7 trillion.

• Internet payments jumped 14.2 percent to 5.9 billion with a total value of $2.9 trillion.

• Payments from health plans to medical and dental providers increased 11.5 percent to 306.7 million with a total value of $1.59 trillion.

• Person-to-person (P2P) payments spiked 32.2 percent to 128.7 million for a total value $209.6 billion.

A recent survey conducted by TD Bank showed treasury and finance professionals anticipate more operational challenges in 2019 than in previous years.

And a separate analysis distributed by Frost & Sullivan highlighted that technologies such as machine learning, big data and blockchain will become prominent, especially as cybercrime becomes more sophisticated and even a method of warfare.

According to an endeavor orchestrated by TD Bank during the 2018 Association for Financial Professionals annual conference in Chicago late last year, the risk of payments fraud and cybersecurity topped professionals’ list of concerns with 44 percent naming it their top operational challenge. That response level presented a 14 percent year-over-year increase.

TD Bank found the ability to adapt to or process faster or electronic payments is an obstacle for 37 percent of survey respondents, also rising 14 percent year-over-year. The bank acknowledged this concern is likely to cause some anxiety for finance professionals, as commercial payments continue evolving.

In fact, the majority (60 percent) of respondents expect to see the largest amount of growth this year within faster or real-time processing, an 8 percent increase from last year.

Despite industry uncertainties, blockchain has benefits

Unsurprisingly, the TD Bank findings showed that technology continues to influence treasury operations, and the majority of survey respondents (90 percent) feel that blockchain/distributed ledger technology will have some type of positive effect on the payments industry.

The top impact of blockchain/distributed ledger technology is its ability to create stronger audit trails (29 percent), respondents said. Additional positive outcomes include:

— Speeding up the payments process (22 percent)

— Improving efficiency of cross-border payments (21 percent)

— Reducing payments fraud (18 percent)

“Blockchain technology has broad implications for the commercial payments space, from speeding up settlements to securing cross-border transactions,” said Rick Burke, head of corporate products and services at TD Bank.

“Even though much of the industry has a baseline understanding that blockchain can evolve and improve payments, the varied responses indicate that the technology’s specific capabilities and implications are still a great unknown for many finance professionals,” Burke continued.

Despite the hype around new innovations like blockchain, TD Bank found that finance professionals appear to be split on the use of another technology type to facilitate payments: open APIs.

Survey results showed 50 percent of respondents claim that their organization currently uses or is in the process of integrating open APIs into company operations, while 49 percent do not use open APIs, and nearly a quarter of that group does not have plans to do so in the future.

With so much change on the horizon, TD Bank’s survey uncovered that companies are investing in training strategies for several facets of treasury operations. Survey respondents said their organization has training strategies specifically for data and analytics (45 percent), AI and automation (26 percent) and blockchain (14 percent).

Fraud casts a larger cloud

As the risk of payments fraud and cybersecurity threats is top of mind across the industry, TD Bank learned that there comes an expectation from 98 percent of respondents that financial institutions should assist organizations with protecting against fraud and cybercrime.

More than half (55 percent) said financial institutions can help them better protect against fraud and cybercrime through education — although 48 percent of respondents admitted that their company does not have any in-house cyber fraud prevention training.

Additionally, TD Bank said one in four finance professionals surveyed feel that banks should offer greater controls on transactions, and 18 percent state they want risk or process reviews.

“As global fraud and cybersecurity incidents continue to rise, corporations recognize the need to bolster their protective measures and improve employee understanding of how to safeguard finances,” Burke said.

“To achieve real success, organizations and their employees need to be better able to identify and deter fraud attempts. This should be a responsibility shared by businesses and their financial institutions, beginning with better education,” he went on to say.

TD Bank polled finance professionals at the 2018 AFP Conference held last November in Chicago. A total of 406 responses were collected from industry professionals, including business end-users and financial and technology services organizations.

More discussion about machine learning and blockchain

Experts at Frost & Sullivan highlighted that machine learning aids early detection of anomalies, while blockchain creates a trustworthy network between endpoints,

The firm also pointed out the rise of the Internet of Things (IoT) has opened up numerous points of vulnerabilities, compelling cybersecurity companies, especially startups, to develop innovative solutions to protect enterprises from emerging threats.

“Deploying big data solutions is essential for companies to expand the scope of cybersecurity solutions beyond detection and mitigation of threats,” Hiten Shah, a research analyst at TechVision, said in the Frost & Sullivan report available here.

“This technology can proactively predict breaches before they happen, as well as uncover patterns from past incidents to support policy decisions,” Shah continued.

Frost & Sullivan’s recent analysis titled, “Envisioning the Next-Generation Cybersecurity Practices,” presents an overview of cybersecurity in enterprises and analyzes the drivers and challenges to the adoption of best practices in cybersecurity. It also covers the technologies impacting the future of cybersecurity and the main purchase factors.

“Startups need to make their products integrable with existing products and solutions as well as bundle their solutions with market-leading solutions from well-established companies,” Shah said. “Such collaborations will lead to mergers and acquisitions, ultimately enabling companies to provide more advanced solutions.”

Frost & Sullivan explained that technologies that are likely to find the most application opportunities include:

— Big data: It can enable automated risk management and predictive analytics. Experts think its adoption will be mostly driven by the need to identify usage and behavioral patterns to help security operations spot anomalies.

— Machine learning: It can allow security teams to prioritize corrective actions and automate real-time analysis of multiple variables. Using the vast pools of data collected by companies, machine learning algorithms can zero in on the root cause of the attack and fix detected anomalies in the network.

— Blockchain: The data stored on blockchain cannot be manipulated or erased by design. Experts explained the tractability of activities performed on blockchain is integral to establishing a trustworthy network between endpoints. Furthermore, the decentralized nature of blockchain greatly increases the cost of breaching blockchain-based networks, which can discourage hackers.

Whether a consumer is buying a personal care item costing just a few bucks or financing a vehicle purchase involving thousands of dollars, Experian insisted that digital commerce has changed the way consumers interact with businesses. Experts see how commerce is moving from face-to-face transactions to anonymous relationships built on trust.

Difficult to achieve and earned over time, Experian sees trusted online relationships are based on businesses providing a secure environment and a great customer experience.

In light of that backdrop, Experian’s Global Identity and Fraud Report found that 74 percent of consumers see security as the most important element of their online experience, followed by convenience.

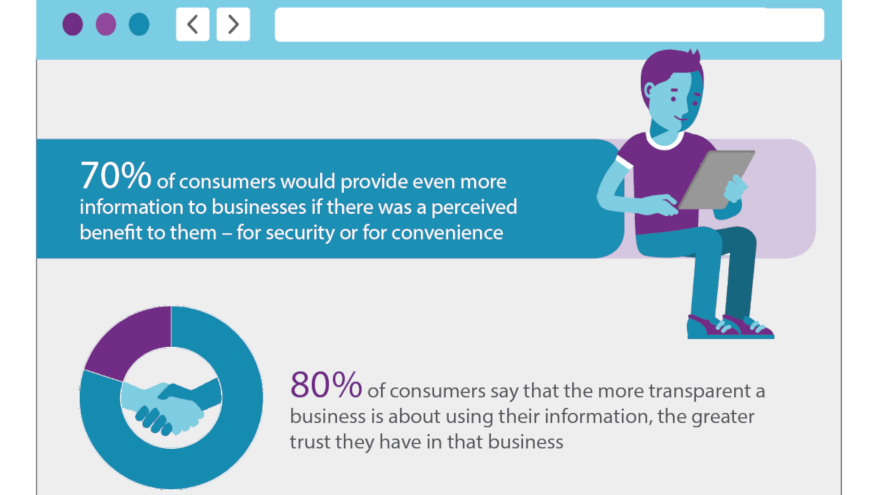

While businesses often have invested in one at the expense of the other, Experian discovered that consumers across the globe expect both. So much so that 70 percent of them are willing to share more personal data with the organizations they interact with online, particularly when they see a benefit such as greater online security and convenience.

“Security and convenience are the bedrocks of a dynamic digital marketplace that effectively manages risk and delivers a seamless experience,” said Steve Pulley, Experian’s executive vice president and general manager of global identity and fraud solutions.

“The availability of information consumers share with businesses makes this possible, but it’s the same information that puts them at a greater risk for fraud, making trust more important than ever,” Pulley continued.

Findings from the study also reveal that consumers and business leaders agree that security methods enabled by new technologies and advanced authentication solutions instill online trust.

In fact, consumer confidence grew from 43 percent to 74 percent when physical biometrics was used to protect their accounts.

Experian learned that businesses also are beginning to embrace the changing technology. Half of organizations globally reported an increase in their fraud management budget over the past 12 months.

“Trust begins with a business’s ability to deliver more from the information they already have and to use advanced technologies to identify their customers and provide a relevant experience without increasing their risk exposure,” Pulley said.

“In other words, consumers really can expect both — security and convenience.”

The report went on to discuss how many businesses are proactively sharing with customers how they use their personal information. The report found that nearly 80 percent of consumers say the more transparent a business is about the use of their information, the greater trust they have in that business.

The report revealed that 56 percent of businesses plan to invest more in transparency-inspired programs such as educating consumers, communicating terms more concisely and helping consumers feel in control of their personal data.

To develop the study, Experian interviewed more than 10,000 consumers and more than 1,000 businesses across 21 countries around the world.

Additional findings from the third annual fraud report include:

• Fifty-five percent of businesses reported an increase in fraud-related losses over the past 12 months, particularly account opening and account takeover attacks.

• Sixty percent of consumers globally are aware of the risks involved with providing their personal information to banks and retailers online.

• Ninety percent of consumers are aware that businesses are collecting, storing and using their personal information.

• Banks and insurance companies are the organizations trusted most by consumers across most regions. Online retail sites and social media sites trail considerably on trust.

• Nearly nine out of 10 consumers report conducting personal banking as their top online activity.

• Passwords, PIN codes and security questions remain the authentication methods most widely used by businesses, followed by document verification, physical biometrics and CAPTCHA.

The Global Identity and Fraud Report also shows how different regions across the globe view and manage fraud:

• Concern for fraud and increased fraud losses are highest among businesses in the U.S.

• The greatest number of consumers who already have experienced a fraudulent event online are in the U.S., with the lowest number of consumers from EMEA.

• The U.S. and the U.K. lead with the biggest increase in fraud management budgets over the past 12 months, with three-quarters of businesses budgeting more for fraud management this year.

• Latin America is a top user of advanced authentication technology where CAPTCHA, physical biometrics and customer identification programs make up the top three authentication methods. This differs for businesses in other regions, which rely more heavily on passwords, PIN codes and security questions.

• Physical biometrics seems to have the largest positive impact on trust, particularly in Colombia and the U.S.

• The U.S. has invested the most when it comes to transparency initiatives in the past 12 months, and Colombia has the highest intent to invest more in the next six months.

Experian’s identity and fraud business comprises more than 300 fraud experts around the world working to protect people’s identities and fight fraud for businesses across multiple sectors, including financial services, telecommunications, retail/e-commerce, insurance, government and healthcare.

The full Global Identity and Fraud Report can be downloaded here.

Artificial intelligence appears to be generating some real revenue in the automotive space.

Coinciding with a major update to its flagship platform, AI-driven marketing automation platform Outsell also announced strong 2018 financial results, with direct revenue up 45 percent over 2017 and direct bookings up 28 percent.

“AI-based marketing solutions are in high demand as dealers seek to individualize their customer communications to enhance the overall customer experience,” said Mike Wethington, founder and chief executive officer of Outsell.

“Outsell was the first to bring AI to auto marketers, and we are well established as the technology leader in the space,” continued Wethington, who insisted that Outsell offers the best platform for definitively measuring the impact of every marketing dollar invested.

Other company highlights from the year included:

• Launching Outsell 5.0, enhanced with even more artificial intelligence capabilities, providing dealers with insight into buying behavior and the ability to take targeted content to the next level, with automated, multi-channel campaigns that are individualized to each person’s exact preferences

• Launching Outsell 5.1, an upgrade that makes Outsell the first to auto-generate individualized customer incentives proven to drive store visits and sales

• Winning 10 awards for its products and its work with customers and partners, including the 2018 WebAward Automobile Standard of Excellence Award, a Gold Stevie Award and a Gold 2018 Summit Creative Awards

“In 2018, we made major improvements to the Outsell platform, laying the groundwork for all kinds of enhancements in 2019,” Wethington said. “At NADA, we announced Outsell 5.2, with new features that make it not only the best solution for managing and optimizing cross-channel marketing campaigns, but also greatly enhance auto marketers’ ability to create and share engaging content especially in social media channels.

“We are also working on some exciting enhancements around what we call private incentive offers that will help dealers provide the right incentives to motivate each individual customer without over-incentivizing — critical in an industry where dealers often spent four to five times as much on incentives as they do on advertising,” he went on to say.

As Wethington mentioned, at the NADA Show 2019 in San Francisco, the company shared details about Outsell 5.2, which he said includes new features for managing and optimizing cross-channel marketing campaigns, but also can enhance auto marketers’ ability to create and share engaging content especially in social media channels.

“Dealers struggle to measure ROI on marketing investments,” Wethington said. “In a competitive environment — and most dealers agree the economy has become more challenging over the past year – Outsell is an essential tool for helping auto marketers optimize results and the effectiveness of each marketing dollar.”

Specific enhancements in Outsell 5.2 include:

• The ability to create and execute on-demand campaigns for specific audiences

• Private offers that dynamically include personalized test-drive, sales and service incentives in email campaigns

• Direct mail integration, for true integration between online and offline campaigns

• Inclusion of new channels — display ads and direct mail on existing Conquest product — to drive increased reach and conversion

• New social ads features including Facebook Marketplace tools and the ability to promote specific inventory in social ads

• New content management capabilities that really separate Outsell from the pack – including new templates, brand compliance tools and the ability to measure/optimize content performance.

Outsell also gathered its Customer Advisory Board during the NADA Show 2019, bringing together dealer marketing leaders to discuss 2019 trends, long-term objectives, and how Outsell can improve its value to dealers.

“Outsell’s CAB meetings are the most valuable meetings we have all year long,” Wethington said. “We get to hear directly from customers about their objectives and challenges. The learnings from these events have a big impact on Outsell’s roadmap every year.”