Carvana already boasted a strong relationship with Ally Financial to help the e-commerce platform for buying and selling used vehicles.

And on Wednesday, Carvana confirmed it now has a connection with Bank of America, too.

According to a news release, the Bank of America digital car shopping and financing platform will now add more than 15,000 Carvana Certified vehicles to its existing inventory of both new and used vehicles available via dealers across the country.

“We always want to give our customers an exceptional experience, whether they finance with Carvana or work with their own banks,” Carvana founder and chief executive officer Ernie Garcia said.

“We look forward to introducing even more Bank of America customers to the new way to buy a car now that they can apply their Bank of America financing to our vehicles on the bank’s digital car shopping platform,” Garcia continued.

Customers simply can visit Bank of America’s digital shopping tool from a computer or mobile device. Once there, they can select a Carvana vehicle, submit an application to Bank of America for immediate financing terms, finalize the transaction on Carvana.com and even trade-in their current vehicle, all in as little as 10 minutes.

Buyers purchasing a Carvana vehicle can take advantage of Carvana’s as-soon-as-next day delivery and complete their purchase and financing tasks without leaving the comfort of home.

“We launched Bank of America digital car shopping to offer our clients a more convenient and transparent experience – from searching vehicles and dealerships to qualifying for financing all from a desktop or mobile device,” said David Hollodick, senior vice president of consumer vehicle lending at Bank of America.

“With Carvana vehicles added to our platform, our clients can take the process one step further and finalize a purchase without ever leaving home. We are delighted to bring this unique experience to more of our clients,” Hollodick continued.

All Carvana vehicles listed on Carvana.com and on the Bank of America car shopping platform are Carvana Certified, meaning they have all undergone a 150-point inspection, have no frame damage and have never been in a reported accident. Features, imperfections and updated information about open safety recalls are listed on the unit’s vehicle description page.

Additionally, every Carvana vehicle comes with a seven-day return policy, giving the customer the time to ensure the vehicle fits their life.

“Whether it’s installing car seats or testing the turning radius in a tight parking garage at work, it’s an upgrade to the traditional four right-hand turns around a dealership block,” Carvana said.

Vinli landed new funding this week that executives say will enable the company to broaden its mobility services and integrations to customers worldwide.

The connected car and data intelligence platform provider announced on Tuesday it has closed $13.5 million in additional funding. The Series B funding round has participation from new and existing investors, including global electric utility provider E.ON, The Westly Group, Hersh Family Investments and Hal Brierley.

The company said Konrad Augustin, investment director at E.ON Scouting and Co-Investments, and Kenneth Hersh, will join Vinli’s board of directors.

Vinli highlighted that it is now on the fast track to add electric vehicles to its growing list of platform capabilities and expand its innovative data intelligence platform, Era.

The company described Era as a revolutionary machine learning platform that can facilitates the streaming from any data source into a secure and intelligent location. The outcome of this technology is increased transparency of data, predictive visibility and flexibility for real-time business and consumer insights.

As Vinli put it, Era is “what smart companies want with their smart vehicle solutions.”

Vinli chief executive officer Mark Haidar elaborated about what the latest funding injection means.

“The investment validates our place in the industry. In the last five years, we have seen the industry unfold and evolve into an industry driven by digital services,” Haidar said. “Companies today need viable data solutions — not only to support the growing number of data sources, but to deliver on the multiple service offerings to their end customers.

“We’re focused on making it easier for large fleets and automakers to access smarter data intelligence,” he continued. “It’s in helping those partners scale and be successful is what we look forward to most at Vinli.”

The company went on to mention the investment deepens the strategic partnership with E.ON, marking Vinli’s first collaboration with an energy company. E.ON will leverage Vinli digital services and data intelligence platform, Era, to broaden electric mobility offerings and tailor solutions for electric fleets.

“With the information from the car itself, we are closing a gap in our data world for eMobilty,” said Frank Meyer, senior vice president innovation and customer solutions at E.ON.

“By combining customer vehicle and network data, we can identify trends at an early stage and will continually create new digital mobility offerings for our customers,” Meyer continued. “Beyond the competitive advantage, we see Vinli as an attractive investment. The company is the global innovation leader in a technology of the future.”

Vinli highlighted the funding round follows a strong fourth quarter of revenue growth, profitability and milestones for the company, including the announcement of Era, and a global strategic partnership with ALD Automotive to make connected services available to its global fleet of 1.6 million vehicles.

With the business in a growth stage, the company added that it will expand across multiple areas. Vinli said it will be making key hires this quarter to fill leadership and engineering roles in the next few months.

Whether a consumer is buying a personal care item costing just a few bucks or financing a vehicle purchase involving thousands of dollars, Experian insisted that digital commerce has changed the way consumers interact with businesses. Experts see how commerce is moving from face-to-face transactions to anonymous relationships built on trust.

Difficult to achieve and earned over time, Experian sees trusted online relationships are based on businesses providing a secure environment and a great customer experience.

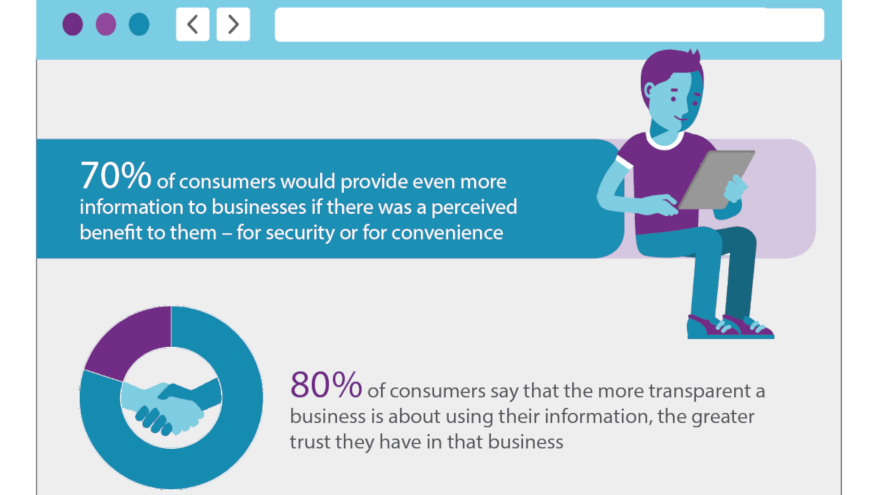

In light of that backdrop, Experian’s Global Identity and Fraud Report found that 74 percent of consumers see security as the most important element of their online experience, followed by convenience.

While businesses often have invested in one at the expense of the other, Experian discovered that consumers across the globe expect both. So much so that 70 percent of them are willing to share more personal data with the organizations they interact with online, particularly when they see a benefit such as greater online security and convenience.

“Security and convenience are the bedrocks of a dynamic digital marketplace that effectively manages risk and delivers a seamless experience,” said Steve Pulley, Experian’s executive vice president and general manager of global identity and fraud solutions.

“The availability of information consumers share with businesses makes this possible, but it’s the same information that puts them at a greater risk for fraud, making trust more important than ever,” Pulley continued.

Findings from the study also reveal that consumers and business leaders agree that security methods enabled by new technologies and advanced authentication solutions instill online trust.

In fact, consumer confidence grew from 43 percent to 74 percent when physical biometrics was used to protect their accounts.

Experian learned that businesses also are beginning to embrace the changing technology. Half of organizations globally reported an increase in their fraud management budget over the past 12 months.

“Trust begins with a business’s ability to deliver more from the information they already have and to use advanced technologies to identify their customers and provide a relevant experience without increasing their risk exposure,” Pulley said.

“In other words, consumers really can expect both — security and convenience.”

The report went on to discuss how many businesses are proactively sharing with customers how they use their personal information. The report found that nearly 80 percent of consumers say the more transparent a business is about the use of their information, the greater trust they have in that business.

The report revealed that 56 percent of businesses plan to invest more in transparency-inspired programs such as educating consumers, communicating terms more concisely and helping consumers feel in control of their personal data.

To develop the study, Experian interviewed more than 10,000 consumers and more than 1,000 businesses across 21 countries around the world.

Additional findings from the third annual fraud report include:

• Fifty-five percent of businesses reported an increase in fraud-related losses over the past 12 months, particularly account opening and account takeover attacks.

• Sixty percent of consumers globally are aware of the risks involved with providing their personal information to banks and retailers online.

• Ninety percent of consumers are aware that businesses are collecting, storing and using their personal information.

• Banks and insurance companies are the organizations trusted most by consumers across most regions. Online retail sites and social media sites trail considerably on trust.

• Nearly nine out of 10 consumers report conducting personal banking as their top online activity.

• Passwords, PIN codes and security questions remain the authentication methods most widely used by businesses, followed by document verification, physical biometrics and CAPTCHA.

The Global Identity and Fraud Report also shows how different regions across the globe view and manage fraud:

• Concern for fraud and increased fraud losses are highest among businesses in the U.S.

• The greatest number of consumers who already have experienced a fraudulent event online are in the U.S., with the lowest number of consumers from EMEA.

• The U.S. and the U.K. lead with the biggest increase in fraud management budgets over the past 12 months, with three-quarters of businesses budgeting more for fraud management this year.

• Latin America is a top user of advanced authentication technology where CAPTCHA, physical biometrics and customer identification programs make up the top three authentication methods. This differs for businesses in other regions, which rely more heavily on passwords, PIN codes and security questions.

• Physical biometrics seems to have the largest positive impact on trust, particularly in Colombia and the U.S.

• The U.S. has invested the most when it comes to transparency initiatives in the past 12 months, and Colombia has the highest intent to invest more in the next six months.

Experian’s identity and fraud business comprises more than 300 fraud experts around the world working to protect people’s identities and fight fraud for businesses across multiple sectors, including financial services, telecommunications, retail/e-commerce, insurance, government and healthcare.

The full Global Identity and Fraud Report can be downloaded here.

Since blockchain is establishing its presence in the automotive sector, strategy and marketing consultancy Simon-Kucher & Partners projected after dissecting recent study findings that the revenue potential for this technology could ramp up to be nearly $120 billion by 2030.

Simon-Kucher orchestrated a survey to delve deeper into what’s prompting car owners and other road users to be interested in the many ways in which blockchain can be used to create revenue opportunities. The firm learned that survey participants were particularly interested in time-saving solutions such as traffic congestion management (48 percent) and automated payments (54 percent).

The firm’s newest blockchain research also mentioned applications that provide added security such as protected data access (50 percent), enable increased efficiency such as automated payments (54 percent), or greater convenience such as remote access (46 percent) were also popular with participants.

“The added value of blockchain applications for the end customer is obvious,” said Peter Harms, a partner in Simon-Kucher’s global automotive practice. “Automakers need to be aware that they can generate significant profit from these applications.”

The study also revealed how much drivers would be willing to pay each month for various blockchain solutions:

—Traffic congestion management: 27 percent of survey participants would be willing to pay on average $11 per month for this solution

— Protected data access: $11 (7 percent)

— Remote control of vehicle (such as locking/unlocking): $8 (12 percent)

— Automated payments (such as at parking or charging stations): $7 (17 percent)

— Immutability of vehicle records (when buying a used vehicle): $6.00 (7 percent)

Based on these figures, Harms computed that total revenue generated by 2030 is set to reach $120 billion.

“The added value of blockchain solutions and customer willingness to pay for them already indicate enormous monetizing potential,” Harms said. “Now is the time for the automotive industry to start adjusting its strategies and business models, not only to expand their current offerings with blockchain solutions but also to monetize them.”

To accomplish this feat, Harms pointed out industry-wide infrastructure is required.

“Close cooperation among individual stakeholders (e.g. automotive manufacturers, taxi companies, municipal corporations, toll operators) is essential to unlock the multi-billion-dollar potential of this technology,” he added.

The study titled, “Blockchain in the Automotive Industry,” was conducted worldwide in October by Simon-Kucher & Partners. It surveyed various factors, including participants’ level of awareness of blockchain, future areas of application in the automotive industry, and willingness to pay for individual applications.

Founded in 1985, Simon-Kucher & Partners has more than 30 years of experience providing strategy and marketing consulting with a focus on top-line power. The firm has more than 1,200 employees in 38 offices worldwide.

RouteOne said on Thursday that one of its longest-tenured executives — chief operating officer Brad Rogers — announced his resignation to take leadership of an organization in an adjacent industry.

And it appears it’s going to take five other RouteOne executives to handle the chores overseen by Rogers, who had been with the company since its inception back in 2002.

As a result of Rogers’ departure, the company indicated his work portfolio will be assumed by expanding the responsibilities of RouteOne’s current leadership team as follows:

— Chris Irving, chief technology officer, will add oversight of the business intelligence team, and continue to lead IT operations, application delivery, architecture, and internal IT systems.

— Jeff Belanger, senior vice president of business development, will add the OEM and strategic alliance teams to his current responsibilities of dealer and finance source relationships, giving him responsibility over all of RouteOne’s business development activities.

— Amanda George will assume responsibility for RouteOne’s marketing team and be elevated to senior vice president, product, customer solutions, integrations, and marketing.

— Jason Bolduc will add the business operations team to his current portfolio of customer success and strategic planning teams and assume the title of vice president, strategy and operations.

— Anthony Goulbourne will be elevated to president of Canadian operations.

All of those five executives will report directly to chief executive officer Justin Oesterle, according to a news release sent by the company.

“Brad Rogers has done a remarkable job with and for RouteOne since its inception in 2002. His leadership has helped form and enable our strategy. We thank him for his contributions and wish him the very best as he pursues his new venture,” Oesterle said.

“We are equally enthusiastic for the growth opportunity this change presents for our leadership team,” Oesterle continued. “RouteOne is fortunate to have an incredibly talented team and we are excited for this next chapter in our journey.”

Separately, RouteOne noted the IT team will be making the following moves:

Rotating their assignments, Maureen Foley will now be director of IT operations and Suren Edara will now be director of application development in an effort to benefit the overall continuity at RouteOne.

3 platform enhancements

Ahead of Thursday's executive announcement, RouteOne highlighted improvements to its eContracting platform that’s supported by more than 7,900 dealers and 60 finance sources.

Coming this year, RouteOne indicated dealers will have access to an expanded digital library of universal deal forms, including odometer statements and title application, along with the ability to create custom forms that are unique to a dealer’s business.

The company explained that deal forms can streamline the vehicle finance transaction by dynamically returning forms that are available for the state in which a dealership conducts business. Form validation can ensure all required fields are complete prior to contract generation and then packages the forms within the electronic signing ceremony.

Meanwhile, RouteOne’s Aftermarket Rating and Contracting Service is a complimentary feature that can allow aftermarket forms to be included within the eContract and the eSigning ceremony.

Currently utilized by 1,700 dealers, RouteOne indicated electronic access to aftermarket providers will greatly expand with the upcoming integration to Open Dealer Exchange’s Provider Exchange Network (PEN) scheduled for 2019. The rating workflow was recently enhanced to enable dealers to electronically begin the aftermarket product registration process on the contract worksheet. This new functionality allows aftermarket products to be rated and specific product(s) selected prior to the finalization and generation the eContract.

RouteOne also mentioned improvements to help vehicle buyers digitally sign the contract package.

RouteOne’s in-dealership electronic signing ceremony no longer requires the purchase of any additional equipment. Following acceptance of an ESIGN Consent and the adoption of a typed or drawn signature, customers can now apply their signature, within the context of the contract, by simply clicking to apply their signature.

The company noted that not only does this new signing experience offer ease of use for the customer, it also can provide the transparency they desire by allowing them to see exactly where they are applying their signature on the contract.

Additionally, RouteOne’s Remote eSigning experience can provide an optimal consumer and dealer experience and robust process flexibility by enabling remote delivery to the consumer of a secure and compliant “signable” financing or lease eContract package, including ancillary documents.

RouteOne’s Remote eSigning is now supported by seven major finance sources.

Furthermore, RouteOne now offers a complimentary, flexible feature to dealers in Arizona, California and Nevada that can allow them to change the original finance source on an eContract, commonly known as Spot, with a simple click of a button even after the customer has reviewed and signed the contract.

This feature’s benefits include the ability to submit such “spot buys” to eligible finance sources electronically and more efficiently with no need for customer re-contracting or papering out.

IHS Markit is leveraging its scale in the economic and technological worlds to help banks and finance companies navigate significant accounting changes coming within the next year.

The company announced the launch of its economic and financial scenario solution designed to help banks comply with the Current Excepted Credit Loss (CECL) estimation required under the Financial Accounting Standards Board (FASB) standard going into effect in 2020.

IHS Markit explained that CECL requires lending institutions to calculate expected credit losses using reasonable and supportable forward-looking macroeconomic and financial forecasts and report the losses on a quarterly or monthly basis. The company contends many firms lack the macroeconomic and financial forecasts, historical macro data and tools required to simulate the range of credit loss scenarios required by CECL.

The IHS Markit solution provides eight economic scenarios to help banks estimate future expected credit impairment, understand risks impacting credit losses and comply with the requirements under CECL. The scenarios are produced by the firm’s award-winning team of economists, using its proprietary, widely-respected macroeconometric model, applied by clients for forecasting and compliance purposes for decades.

“Our CECL solution provides the macroeconomic and financial scenarios and historical data to drive a firm’s credit loss estimates, whether produced in house or by a third-party,” said Chris Varvares, vice president and co-head of U.S. economics at IHS Markit. “It delivers eight transparent and comprehensive, probability-weighted macroeconomic and financial scenarios from our proprietary models and is able to be implemented across many vendor platforms firms already employ.”

Specifically, the solution includes:

— National macro and financial data: Historical and forecast data for eight scenarios at a national level

— Regional data: Historical and forecast data for three scenarios covering nine regions, 50 states and the top 100 metropolitan areas

The forecasts are provided over a 10-year horizon and are updated monthly. The scenarios are accessible through the Connect Platform from IHS Markit or able to be implemented across various vendor platforms.

The eight scenarios include the Macroeconomic Advisers by IHS Markit baseline forecast, representing the most likely scenario, three scenarios with better outcomes in terms of near-term growth and four scenarios with worse outcomes.

Among the current scenarios are faster growth/rapid productivity, boom/bust and global slump/financial crisis. Providing seven alternative scenarios can give banks options for choosing scenarios that best fit their needs.

Macroeconomic Advisers by IHS Markit was recently named the most accurate U.S. economic forecaster for 2017 by the Wall Street Journal and Focus Economics. Nariman Behravesh and the IHS Markit U.S. macroeconomic team also received the 2017 Lawrence R. Klein Award for forecasting accuracy.

For more information, managers and executive can listen to a recent webinar hosted by Varvares and the HIS Markit team.

Funds to help fintech firms in Europe arrived on Monday.

Fintech business lender MarketInvoice announced it has raised 26 million euros in new equity funding. This Series-B funding round was led by Barclays and fintech fund Santander InnoVentures with significant participation from European venture fund Northzone, an existing investor in the company.

Technology credit fund Viola Credit, who also participated in the equity round, will provide a debt facility of up to 30 million euros to help scale the MarketInvoice business loans solution that sits alongside its core invoice finance solutions.

Since 2011, MarketInvoice has funded invoices and business loans to United Kingdom companies worth more than 2 billion euros, making them one of Europe’s largest online invoice finance platforms. MarketInvoice has supported thousands of companies across the U.K., funding more than 170,000 invoices and supporting over 15,000 U.K. jobs, by providing business finance to help them grow, expand operations and hire more people.

Executives explained the funding will enable MarketInvoice to deepen strategic partnerships in the U.K., grow the team and increase awareness of its business finance solutions. In addition, the company is planning to launch cross-border fintech-bank partnerships to support more businesses with access to its lending solutions.

MarketInvoice co-founder and chief executive officer Anil Stocker said, “This investment is perfectly timed for the company. The quality of investors we are bringing in through this funding round is a real testament to the whole team at MarketInvoice and the value we are building.

“We’re excited to develop our finance solutions further and become the trusted funding partner for ambitious entrepreneurs,” Stocker continued. “By collaborating with bank partners, we will be reaching many thousands of companies here in the U.K. and abroad to provide them with their business finance needs.

“We aim to invest in technology, data and strategic partnerships, to take MarketInvoice to the next level,” Stocker went on to say.

Santander InnoVentures managing partner and head of investments Manuel Silva Martinez evaluated why the company made this move.

“MarketInvoice is helping U.K. businesses access much needed funding to keep their businesses and ideas thriving in a very competitive market,” Silva Martinez said. “We are pleased to be joining other financial institutions as shareholders to scale their solutions in the U.K. and abroad. We are very excited to join Anil and his exceptional team in building this vision together.”

Ian Rand, CEO of Barclays Business Bank, shared his assessment of the investment, too.

“Collaborating with fintech companies like MarketInvoice is an integral part of Barclays’ strategy for accelerating growth,” Rand said. “This investment demonstrates our commitment to the partnership we announced last summer which offers hundreds of thousands of our SME clients access to even more innovative forms of finance, boosting cash flow and competition in the market.”

Furthermore, Viola Credit partner Ido Vigdor, addressed the development, as well.

“More than 6 billion euros has been funded through alternative finance lending in the U.K. and it has become an established mainstream component in the U.K. financial landscape,” Vigdor said.

“The awareness, adoption and impact of alternative finance options are increasing rapidly as platforms, such as MarketInvoice, are providing seamless, easy to use, financial services. We are excited to enter the U.K. market and partner with this exceptional company as it enters to it next phase of growth,” Vigdor went on to say.

Finally, Stocker added more insight about what the additional financial resources could do.

“Now more than ever, businesses need access to stable lines of funding as they navigate choppy political and economic conditions. Our invoice finance solutions are designed to bridge the gap in cash flow requirements and keep UK businesses growing and exporting,” Stocker said.

“We will use this new funding to invest in further risk automation and data models, scale-up our business loans solution and grow our teams,” Stocker continued.

Major consolidation in the fintech space unfolded on Wednesday.

Fiserv and First Data Corp. announced that their boards of directors have unanimously approved a definitive merger agreement under which Fiserv will acquire First Data in an all-stock transaction. The companies said the transaction unites two premier firms to create one of the world’s leading payments and financial technology providers and an enhanced value proposition for its clients.

According to a news release, the transaction, which is expected to close during the second half of 2019, is subject to customary closing conditions and regulatory approvals, including the approval of shareholders of both companies. The transaction is not subject to any financing conditions.

Under the terms of the agreement, First Data shareholders will receive a fixed exchange ratio of 0.303 Fiserv shares for each share of First Data common stock they own, for an equity value of $22 billion. This represents $22.74 based on closing prices as of Wednesday and a premium of 29 percent to the five-day volume weighted average price as of that date.

Following the close of the transaction, Fiserv shareholders will own 57.5 percent of the combined company, and First Data shareholders will own 42.5 percent, on a fully diluted basis. The all-stock transaction is intended to be tax-free to First Data shareholders, according to the companies.

Executives highlighted this highly complementary combination will offer leading technology capabilities that enable a range of payments and financial services, including account processing and digital banking solutions; card issuer processing and network services; e-commerce; integrated payments; and the Clover cloud-based point-of-sale solution. The combined company will offer comprehensive distribution channels and have deep expertise in partnering with financial institutions, merchants and billers of all sizes, as well as software developers.

“Through this transformative combination, we expect to redefine the manner in which people and institutions move money and information,” said Jeffery Yabuki, president and chief executive officer of Fiserv.

“We admire First Data for its excellence in merchant acquiring and global issuing services, and the tremendous progress they have made under Frank’s leadership. We expect this combination to catalyze and support an enhanced value proposition for our collective clients and their customers,” Yabuki continued.

First Data chairman and chief executive officer Frank Bisignano added, “I have long admired what Fiserv has achieved over the years, and I look forward to working with the talented associates of both companies as we set a higher standard of innovation and service in the industry.

“Our goal at First Data has always been to provide our clients with the most comprehensive suite of innovative, highly-differentiated solutions and services, and I am excited by the significant value that the combination with Fiserv creates for all stakeholders,” Bisignano went on to say.

Wednesday’s announcement indicated the combined company will be led by an experienced board and leadership team that leverages the strengths and capabilities of both companies. Upon closing, the board of the combined company will consist of 10 members, six of whom will be from the board of Fiserv and four of whom will be from the board of First Data.

Upon closing, Yabuki will serve as chief executive officer and chairman of the board of directors of the combined company. Bisignano will assume the role of president and chief operating officer, and will serve as director of the board of the combined company. The combined entity will be known as Fiserv.

“We expect the combined company to retain our current investment-grade ratings based on our strong financial profile and excellent free cash flow. Together, this should provide the basis for continued disciplined capital allocation, including debt repayment and share repurchase,” Yabuki said.

“We look forward to welcoming First Data’s talented associates to Fiserv as we drive the global digitization of payments and financial technology services,” he went on to say.

Deloitte focused on three new technologies in an annual report that highlights on the latest trends that experts described as creating a climate of disruption and uncertainty.

The report titled, “Tech Trends 2019: Beyond the digital frontier,” explored how the convergence of new technologies with powerful forces is driving disruption across industries. According to a recap shared on Wednesday, those new technologies include advanced networking, serverless computing and intelligent interfaces as well as technological forces encompassing digital experiences, cognitive and cloud.

Back 10 years ago, when smartphones and mobile apps were gaining traction, and technologies like cloud and the Internet of Things were emerging on the scene, Deloitte released its first Tech Trends report. The organization has watched this evolution unfold as the digital imperative and the changing role of technology redefine the enterprise, yet adoption of these trends continues to vary widely.

Experts noted that some companies are only beginning to explore trends Deloitte wrote about in 2010, while others have advanced rapidly along the maturity curve.

“Make no mistake: Technology is not just an enabling function. Tech is the universal language of business today,” said Bill Briggs, global and U.S. chief technology officer for Deloitte Consulting.

“As the pace of change quickens, technology now leads business strategy. And technology trends has evolved from a CIO (chief information officer) and CTO (chief technology officer) concern into something driving CEO, management team, boardroom agendas — to redefine what enterprises can accomplish,” Briggs continued.

Authors recapped that “Tech Trends 2019: Beyond the digital frontier,” begins with a reflection on a decade of disruptive change driven by nine macro forces: digital experience, analytics, cloud, core modernization, cyber, business of information technology, cognitive, blockchain, and digital reality. The report further explores where these forces are headed.

Next, six trends that are giving rise to new operating models, redefining the nature of work and dramatically changing IT’s relationship with the business are detailed, including:

— AI-fueled organizations: Leading companies are systematically deploying rapidly maturing technologies — machine learning, natural language processing, robotic process automation (RPA) and cognitive — not just to every core business process, but into products, services and the future of industries. Deloitte believes organizations’ use of artificial intelligence is moving from “Why?” to “Why not?”

— NoOps in a serverless world: Experts asserted we’ve reached the next stage in the evolution of cloud computing with technical resources completely abstracted and management tasks increasingly automated. Freed from mundane responsibilities, the report noted IT talent can focus on activities that more directly support business outcomes.

— Connectivity of tomorrow: At both macro and micro levels, Deloitte explained technologies like 5G, mesh networks and edge computing are expanding business’ reach to both the far corners of the world — and the smallest spaces in warehouses, retail stores and other places with utmost precision. Experts contend that advanced networking is the “unsung hero,” driving development of new products and services and is transforming how work gets done.

—Intelligent interfaces: Today, Deloitte pointed out that people interact with technology through ever more intelligent interfaces that combine the latest in human-centered design techniques with leading-edge technologies such as computer vision, conversational voice, auditory analytics, augmented reality and virtual reality. Working in concert, experts see these technologies and techniques are transforming the way we engage with machines, data and each other.

— Beyond marketing with a reimagined experience: To deliver the highly personalized, contextualized experiences that today’s customers expect, Deloitte mentioned that some chief marketing officers are trading long-standing, traditional agency relationships for closer partnerships with their own CIOs. Enabled by a new generation of marketing tools and techniques focused on personalized, contextual and dynamic experiences, experts indicated that CIOs and CMOs can illuminate and engage customer needs and desires most effectively.

— DevSecOps and the cyber imperative: Deloitte explained that DevSecOps fundamentally can transform cyber, security, privacy and risk management from being compliance-based activities — typically undertaken late in the development lifecycle — into essential framing mindsets across the product journey.

The report closes by exploring how modern businesses can navigate digital transformation — building a roadmap that incorporates the right technologies, techniques, talent and executive support.

“While we take a pragmatic view, we also aspire to understand fully how forces like serverless technology, connectivity capabilities, and intelligent interfaces are reshaping industries,” said Scott Buchholz, managing director and government and public services chief technology officer at Deloitte Consulting.

“The report details how organizational leadership can shape ambitions and instill a culture to sense and make sense of what tomorrow may bring. And – importantly – a path to get there from the realities of today,” Buchholz went on to say.

The entire report can be downloaded here.

A trio of connected global OEMs is pushing more resources into streamlining the vehicle-purchase process with improved, cloud-based technology.

Alliance Ventures, the strategic venture capital arm of Renault-Nissan-Mitsubishi, announced a new investment in digital technologies and services by investing in Tekion, a U.S. company that seeks to bring connected digital experiences to automotive retail through machine learning and artificial intelligence capabilities.

According to a news release sent on Wednesday, financial terms of the Tekion investment will not be disclosed.

Officials did share that the investment in Tekion, based in California’s Silicon Valley, is the latest investment by Alliance Ventures in start-ups, early-stage development and entrepreneurs at the cutting edge of next-generation systems for the automotive industry.

“At Tekion, we offer the latest technology from ML/AI to big data and internet of things, all integrated in one cloud platform, bringing a seamless digital experience from online to in-store,” Tekion founder and chief executive officer Jay Vijayan.

“This investment from Alliance Ventures will enable us to go farther and faster in creating best-in-class, integrated experiences that connect OEMs, dealers, and consumers better than ever before,” Vijayan continued.

This investment by Alliance Ventures to start the year follows nine other direct investments in 2018 in startups based in North America, Europe, Middle-East and China in an effort to contribute to the future of mobility for all.

“Renault-Nissan-Mitsubishi believes that automotive groups with the most advanced and digitally-connected customer services will enjoy significant competitive advantages,” Alliance Global vice president of ventures and open innovation François Dossa said.

“This is one of the reasons we are investing in Tekion, a company that is leveraging the most advanced technologies to provide digital experiences and solutions for automotive retail,” Dossa went on to say.