Perhaps now Equifax, along with federal and state regulators, can close the chapter of the company’s history that included the 2017 data breach.

On Monday, the credit bureau announced a comprehensive $671 million resolution that includes settlement agreements that would resolve the multi-district consumer class action litigation, as well as investigations by the Federal Trade Commission, the Consumer Financial Protection Bureau, the attorneys general of 48 states, Puerto Rico and the District of Columbia and the New York Department of Financial Services (NYDFS).

If approved by the court, a consumer restitution fund of up to $425 million will be available to pay for three-bureau credit monitoring for consumers whose information was impacted in the 2017 breach, actual out-of-pocket losses related to the breach, and other consumer benefits such as identity restoration services.

Equifax said it has been providing free credit monitoring services to consumers since September 2017.

“This comprehensive settlement is a positive step for U.S. consumers and Equifax as we move forward from the 2017 cybersecurity incident and focus on our transformation investments in technology and security as a leading data, analytics, and technology company,” Equifax chief executive officer Mark Begor said.

“The consumer fund of up to $425 million that we are announcing today reinforces our commitment to putting consumers first and safeguarding their data — and reflects the seriousness with which we take this matter,” Begor continued. “We have been committed to resolving this issue for consumers and have the financial capacity to manage the settlement while continuing our $1.25 billion EFX2020 technology and security investment program. We are focused on the future of Equifax and returning to market leadership and growth.”

In September of 2017, Equifax announced that a data breach at the company resulted in the exposure of approximately 147 million U.S. consumers’ sensitive personal information, including names, addresses, Social Security Numbers and dates of birth. The bureau coordinated its investigation with the FTC and attorneys general from across the country.

In total, the settlements with these entities would impose up to $700 million in relief and penalties.

Investigation and breach details

The FTC alleged that Equifax failed to patch its network after being alerted in March 2017 to a critical security vulnerability affecting its ACIS database, which handles inquiries from consumers about their personal credit data. Even though Equifax’s security team ordered that each of the company’s vulnerable systems be patched within 48 hours after receiving the alert, the FTC said Equifax did not follow up to ensure the order was carried out by the responsible employees.

In fact, the FTC said Equifax did not discover that its ACIS database was unpatched until July 2017, when its security team detected suspicious traffic on its network. The regulator recapped that a company investigation revealed that multiple hackers were able to exploit the ACIS vulnerability to gain entry to Equifax’s network, where they accessed an unsecured file that included administrative credentials stored in plain text. These credentials allowed the hackers to gain access to vast amounts of consumers’ personally identifiable information and to operate undetected on Equifax’s network for months.

The hackers targeted Social Security numbers, dates of birth, and other sensitive information, mostly from consumers who had purchased products from Equifax such as credit scores, credit monitoring, or identity theft prevention services. For example, hackers stole at least 147 million names and dates of birth, 145.5 million Social Security numbers, and 209,000 payment card numbers and expiration dates.

Hackers were able to access a “staggering” amount of data because Equifax failed to implement basic security measures, according to the complaint. This includes failing to implement a policy to ensure that security vulnerabilities were patched; failing to segment its database servers to block access to other parts of the network once one database was breached; and failing to install robust intrusion detection protections for its legacy databases.

In addition, the FTC also alleges that Equifax stored network credentials and passwords, as well as Social Security numbers and other sensitive consumer information, in plain text.

Despite its failure to implement basic security measures, Equifax’s privacy policy at the time stated that it limited access to consumers’ personal information and implemented “reasonable physical, technical and procedural safeguards” to protect consumer data.

The FTC also alleged that Equifax violated the FTC Act’s prohibition against unfair and deceptive practices and the Gramm-Leach-Bliley Act’s Safeguards Rule, which requires financial institutions to develop, implement and maintain a comprehensive information security program to protect the security, confidentiality, and integrity of customer information.

“Companies that profit from personal information have an extra responsibility to protect and secure that data,” FTC chairman Joe Simons said in a news release. “Equifax failed to take basic steps that may have prevented the breach that affected approximately 147 million consumers.

“This settlement requires that the company take steps to improve its data security going forward, and will ensure that consumers harmed by this breach can receive help protecting themselves from identity theft and fraud,” Simons said.

More information about the settlement

According to a news release from the CFPB, the bureau alleged in its complaint that Equifax violated the law in several ways through its conduct both before and after the breach. Specifically, the bureau alleged, Equifax engaged in unfair and deceptive practices in violation of the Consumer Financial Protection Act of 2010 by:

— Failing to provide reasonable security for the massive quantities of sensitive personal information stored within its computer network, causing substantial injury to consumers whose data was stolen

— Deceiving consumers about the strength of its data security program in its privacy policies

— Engaging in acts and practices that caused additional harm or risk of harm to consumers in response to the breach.

To provide relief for consumers affected by the breach, the bureau’s proposed order requires Equifax to establish a consumer fund with up to $425 million available to provide affected consumers with a broad array of redress. The consumer fund would be used to provide reimbursements to affected consumers for time and money they spent related to the breach.

If the court approves the settlement, affected consumers may be eligible to receive money by filing one or more claims of up to $20,000 per individual for lost time and money for the following:

— $25 per hour for up to 20 hours for time spent protecting personal information or addressing identity theft after the breach

— Money spent purchasing credit monitoring or identity theft protection after the breach

— The cost of freezing or unfreezing credit reports at any consumer reporting agency after the breach

— Reimbursement for up to 25% of the amount paid to Equifax for credit or identity monitoring subscription products between Sept. 7, 2016 and Sept. 7, 2017

— Any unreimbursed costs, expenses, losses, or charges incurred as a result of identity theft

— Miscellaneous expenses associated with any of the above, such as notary, fax, postage, mileage and telephone charges

The CFPB said all affected consumers would be eligible to receive at least 10 years of free credit monitoring, at least seven years of free identity-restoration services, and, starting on Dec. 31, and extending seven years, all U.S. consumers may request up to six free copies of their Equifax credit report during any 12-month period.

These free copies will be provided to requesting consumers in addition to any free reports to which they are entitled under federal law, according to officials

If consumers choose not to enroll in the free credit monitoring product available through the settlement, the bureau indicated they may seek up to $125 as a reimbursement for the cost of a credit-monitoring product of their choice.

The CFPB noted a settlement administrator will manage the claims process. Consumers must submit a claim in order to receive free credit monitoring or cash reimbursements. After the court approves the settlement, consumers can submit a claim online at www.EquifaxBreachSettlement.com, or by mail. Consumers may visit this website to learn about the deadlines for filing claims.

In addition to consumer relief, Equifax would be required to pay the bureau a $100 million civil money penalty. Equifax also would be required to make significant improvements to its data security practices and would be subject to ongoing oversight by regulators.

“Today’s announcement is not the end of our efforts to make sure consumers’ sensitive personal information is safe and secure,” CFPB director Kathleen Kraninger said.

“The incident at Equifax underscores the evolving cybersecurity threats confronting both private and government computer systems and actions they must take to shield the personal information of consumers,” Kraninger continued. “Too much is at stake for the financial security of the American people to make these protections anything less than a top priority.”

New York heavily involved on state level

New York attorney general Letitia James co-led the coalition of 50 attorneys general in reaching the settlement with Equifax.

“Equifax put profits over privacy and greed over people, and must be held accountable to the millions of people they put at risk,” James said in a news release. “This company’s ineptitude, negligence, and lax security standards endangered the identities of half the U.S. population.

“Now it’s time for the company to do what’s right and not only pay restitution to the millions of victims of their data breach, but also provide every American who had their highly sensitive information accessed with the tools they need to battle identity theft in the future,” James continued.

Additionally, the New York State Department of Financial Services (DFS) separately investigated Equifax’s security practices, and found that the company engaged in practices that violated the Dodd-Frank Act and Financial Services Law 408. As a result, Equifax will be fined an additional $10 million by DFS, bringing the total New York State will receive in fines to more than $19.2 million.

“First and foremost, the settlement announced today holds Equifax accountable for its egregious breach in its duty to consumers in safeguarding their sensitive personal identifying information and restores some peace of mind and protection to New Yorkers,” DFS superintendent Linda Lacewell said.

“Strengthening consumer protections for New Yorkers, DFS now requires credit rating agencies to be licensed and supervised by DFS, and comply with the Department’s landmark cybersecurity regulation to better guard against potential breaches,” Lacewell went on to say.

Some consumer advocates still not happy

U.S. PIRG said the “Equifax penalty is a sweetheart deal that leaves consumers at risk.” U.S. PIRG is the federation of state public interest research groups, which are non-profit, non-partisan public interest advocacy organizations.

“Equifax appears to have made a calculated decision that losing the Social Security Numbers and birth dates of some 148 million consumers to identity thieves was worth only about $700 million or a little less,” U.S. PIRG federal consumer program director Ed Mierzwinski said in a news release distributed late on Friday. “The shelf life of financial DNA is forever so this sounds like a sweetheart deal for a company that failed to do its basic job: protect consumer data.

“Failure to protect privacy has a real harm; we think Equifax should have paid real money, not ‘just go-away’ money, and promised real changes to its sloppy last-century practices,” Mierzwinski continued.

GBG, a U.K.-headquartered identity data intelligence specialist, recently announced that it has conditionally agreed to acquire IDology, a U.S.-based provider of identity verification and fraud prevention services.

The company said the all-cash transaction is for $300 million.

IDology is a fast-growing provider of identity verification services that is designed to help remove friction both in onboarding customers and in the detection of fraud. Officials highlighted its U.S. identity verification and fraud prevention services, led by its ExpectID product range, are the perfect strategic complement to GBG’s identity verification solutions.

“For the past 15 years, IDology has provided multi-layered identity verification. With the combination of IDology and GBG, we intend to innovate, delivering exceptional solutions for our customers, focusing on driving customer revenue and preventing fraud,” IDology president and chief executive officer John Dancu said.

“With GBG’s expertise in global data, we are all excited to expand our solutions and our trusted consortium network for customers across the globe,” Dancu continued.

GBG claims it can quickly validate and verify the identity and location of 4.4 billion people globally and accesses a breadth of data from more than 200 global partners to establish trust between businesses and their customers. Having completed 11 acquisitions since 2011, GBG’s $300 million acquisition of IDology is its largest to date.

GBG has seen strong growth in the U.S. market. Its existing U.S. identity business has grown organically with customers across technology, payments and retail verticals. Meanwhile, Loqate, its location intelligence solution, has offices in New York and San Francisco and has seen high demand from household names like Abercrombie and Fitch, Oracle and Nordstrom.

The acquisition will strengthen GBG’s broader portfolio and enhance the business’ product capability and customer reach.

The companies went on to mention GBG and IDology have a history of working together in partnership and share a similar culture with a strong emphasis on people and talent. IDology’s U.S. customer base currently accounts for 99 percent of its revenue, which will provide GBG with geographic scale and help to position GBG as a global leader in electronic identification verification.

“I am delighted to announce the acquisition of IDology. With attractive organic growth, significant synergies and a strong cultural alignment, this is a high-quality addition to GBG,” chief exeutive officer Chris Clark said. “The combination of IDology and GBG enables us to meet growing customer appetite for an identity verification provider with global capabilities and scale in key markets.

“We are excited by the compelling strategic rationale behind this acquisition,” Clark continued. “It enables GBG to quickly expand even further into North America, a key growth territory for the business. We have already built an exciting domestic presence in the U.S. with Loqate, our location proposition, and IDology now gives us an excellent platform for both identity verification and fraud prevention.

“The board and I look forward to the future success that we anticipate that our combined business can deliver,” Clark went on to say.

Whether a consumer is buying a personal care item costing just a few bucks or financing a vehicle purchase involving thousands of dollars, Experian insisted that digital commerce has changed the way consumers interact with businesses. Experts see how commerce is moving from face-to-face transactions to anonymous relationships built on trust.

Difficult to achieve and earned over time, Experian sees trusted online relationships are based on businesses providing a secure environment and a great customer experience.

In light of that backdrop, Experian’s Global Identity and Fraud Report found that 74 percent of consumers see security as the most important element of their online experience, followed by convenience.

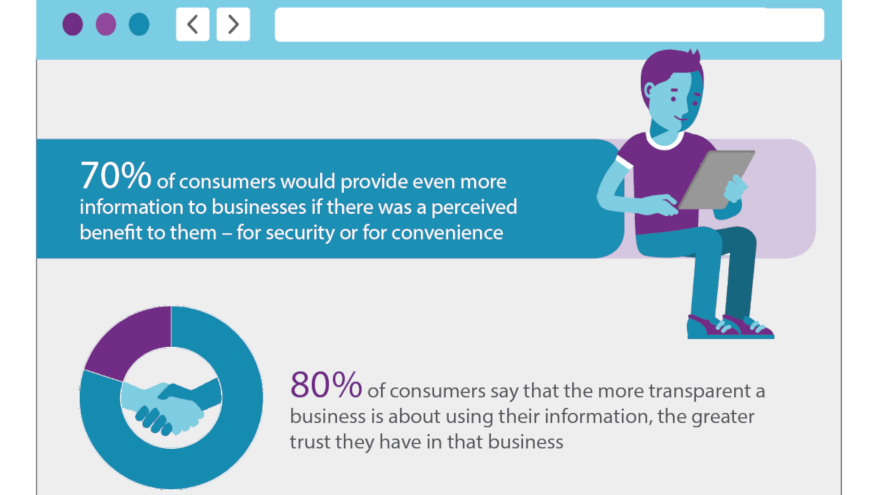

While businesses often have invested in one at the expense of the other, Experian discovered that consumers across the globe expect both. So much so that 70 percent of them are willing to share more personal data with the organizations they interact with online, particularly when they see a benefit such as greater online security and convenience.

“Security and convenience are the bedrocks of a dynamic digital marketplace that effectively manages risk and delivers a seamless experience,” said Steve Pulley, Experian’s executive vice president and general manager of global identity and fraud solutions.

“The availability of information consumers share with businesses makes this possible, but it’s the same information that puts them at a greater risk for fraud, making trust more important than ever,” Pulley continued.

Findings from the study also reveal that consumers and business leaders agree that security methods enabled by new technologies and advanced authentication solutions instill online trust.

In fact, consumer confidence grew from 43 percent to 74 percent when physical biometrics was used to protect their accounts.

Experian learned that businesses also are beginning to embrace the changing technology. Half of organizations globally reported an increase in their fraud management budget over the past 12 months.

“Trust begins with a business’s ability to deliver more from the information they already have and to use advanced technologies to identify their customers and provide a relevant experience without increasing their risk exposure,” Pulley said.

“In other words, consumers really can expect both — security and convenience.”

The report went on to discuss how many businesses are proactively sharing with customers how they use their personal information. The report found that nearly 80 percent of consumers say the more transparent a business is about the use of their information, the greater trust they have in that business.

The report revealed that 56 percent of businesses plan to invest more in transparency-inspired programs such as educating consumers, communicating terms more concisely and helping consumers feel in control of their personal data.

To develop the study, Experian interviewed more than 10,000 consumers and more than 1,000 businesses across 21 countries around the world.

Additional findings from the third annual fraud report include:

• Fifty-five percent of businesses reported an increase in fraud-related losses over the past 12 months, particularly account opening and account takeover attacks.

• Sixty percent of consumers globally are aware of the risks involved with providing their personal information to banks and retailers online.

• Ninety percent of consumers are aware that businesses are collecting, storing and using their personal information.

• Banks and insurance companies are the organizations trusted most by consumers across most regions. Online retail sites and social media sites trail considerably on trust.

• Nearly nine out of 10 consumers report conducting personal banking as their top online activity.

• Passwords, PIN codes and security questions remain the authentication methods most widely used by businesses, followed by document verification, physical biometrics and CAPTCHA.

The Global Identity and Fraud Report also shows how different regions across the globe view and manage fraud:

• Concern for fraud and increased fraud losses are highest among businesses in the U.S.

• The greatest number of consumers who already have experienced a fraudulent event online are in the U.S., with the lowest number of consumers from EMEA.

• The U.S. and the U.K. lead with the biggest increase in fraud management budgets over the past 12 months, with three-quarters of businesses budgeting more for fraud management this year.

• Latin America is a top user of advanced authentication technology where CAPTCHA, physical biometrics and customer identification programs make up the top three authentication methods. This differs for businesses in other regions, which rely more heavily on passwords, PIN codes and security questions.

• Physical biometrics seems to have the largest positive impact on trust, particularly in Colombia and the U.S.

• The U.S. has invested the most when it comes to transparency initiatives in the past 12 months, and Colombia has the highest intent to invest more in the next six months.

Experian’s identity and fraud business comprises more than 300 fraud experts around the world working to protect people’s identities and fight fraud for businesses across multiple sectors, including financial services, telecommunications, retail/e-commerce, insurance, government and healthcare.

The full Global Identity and Fraud Report can be downloaded here.

While facing challenges on multiple fronts, report findings declared that changing customer behaviors and demands should be fueling change in the service and products retail banks are offering. Those assertions arrived as part of an in-depth study released on Wednesday by banking software company Temenos.

The report, written by the Economist Intelligence Unit (EIU) on behalf of Temenos and titled, "Whose customer are you? The reality of digital banking in North America," explored the developing fintech situation for retail banks in North America.

The regional report emphasized the need for North American retail banks to further embrace change by developing their digital marketing and engagement (cited by 53 percent of respondents) and improving product agility (cited by 49 percent).

The report also noted that when it comes to preparing for digital change, American banks, in particular, need to examine the experiences of Europe and Asia-Pacific in creating a one-stop digital journey for their customers. Authors found that those institutions with a global footprint especially can learn from Europe's open banking experience.

Although concerns about regulatory fines and recompense orders are higher in North America (56 percent versus 43 percent globally), the report pointed out there is space for banks to work together to overcome the confusing mesh of federal and state regulations.

The report goes on to note that banks in North America are already beginning to come together to collaborate — a necessary effort in order to build a truly modern banking system that supports innovation.

“North American banks need to be able to respond better to how their customers live now in terms of their digital offerings if they are to remain truly competitive against neo and challenger banks,” said Renee Friedman, editor of the report from the Economist Intelligence Unit.

Other key report highlights included:

—North American bankers see their current business model evolving to develop niche propositions for their clients, more so than their global counterparts do (71 percent versus 61 percent).

—More North American bankers (87 percent) believe that the platformization of banking and other services through a single-entry point will steer the market than their global counterparts (78 percent).

—Retail banks across North America are focusing their digital investment on cyber security (76 percent).

—North American bankers consider conforming to data protection and privacy regulation to be the biggest challenge their company faces concerning data and third-party access (31 percent versus 21 percent globally).

—North American banks’ innovation strategies are focused on investing in fintech start-ups (54 percent).

The Economist Intelligence Unit surveyed 400 global banking executives about the challenges retail banks expect to face between now and 2020, and the strategies they are deploying in response. Orchestrators said 51 percent of respondents were at C-Suite level and 10 percent were board members.

The North America report was based on 100 respondents from North America (the U.S. and Canada) and was supplemented with in-depth interviews with senior executives from leading regional banks.

“Though we have strict regulations in place, nevertheless disruption is happening here in North America. We are seeing exciting developments across the region as the banking industry explores what it means to bank in a digital world,” said Emily Steele, Temenos’ president for North America.

“Incumbent banks are setting up digital banks alongside their own operations, challenger banks are popping up, and now we are starting to see fintechs moving to become banks themselves,” Steele continued.

“Banks are awakening to the need to personalize and contextualize their digital products and services, and offer customers great customer journeys, in order to compete and remain successful,” she went on to say.

The entire report can be downloaded here.

CompliancePoint is looking to find vulnerabilities before data-driven miscreants find a pathway to leverage company information in unsavory ways.

CompliancePoint, a leading provider of information security and risk management services for compliance and data security, recently established a data privacy solutions focus for the automotive industry, with resources to protect manufacturers, auto finance companies, dealers and other users of automotive data.

In 2018, CompliancePoint contends more than 100 automotive manufacturing companies including General Motors, Fiat Chrysler, Tesla, Ford, Toyota and Volkswagen experienced a data breach exposing trade secrets from the OEM.

“Data privacy and trade secrets are crucial components in the automotive industry,” CompliancePoint said. “A data breach can cost millions in monetary value, not including the loss of priceless trade secrets that lead to unfair advantages to competitors when crucial data is compromised.”

According to Forbes, CompliancePoint indicated it can take companies an average of 200 days to identify a data breach, and another 70 days to contain in. CompliancePoint offers cybersecurity assessments to automotive companies, which are designed to prevent potential liabilities and mitigate risk by protecting security framework.

Some key services include mobile and wireless testing, web application testing and data breach attempt response.

“Automotive companies can strengthen their data security, lower operational costs, and simplify their compliance process,” CompliancePoint said.

Vulnerability and penetration testing (PEN Testing) are performed to expose known and unknown weaknesses through experts who attempt to hack the automotive organizations' web systems. PEN tests further identify areas of weakness that put an automotive organization at risk.

CompliancePoint said it can provide a complete cybersecurity solution for automotive organizations through cyber threat assessments and quality results that are crucial to identifying issues that can leave an automaker at risk.

“CompliancePoint further works to resolve found issues, offering a comprehensive yet proactive approach to assessing cyber threats,” the company said. “Risk management provides automotive organizations with monitoring solutions and attentiveness that is needed for real security and peace of mind.”

For more details, go to www.compliancepoint.com.

While the auto finance industry certainly is taking steps to reduce its exposure, the latest analysis from LexisNexis Risk Solutions showed how much rampant fraud still is happening in the greater retail sector.

In fact, findings from its comprehensive "2018 True Cost of Fraud" report indicated fraud is escalating at an “unprecedented” pace within industry segments already operating on very thin margins.

The LexisNexis Fraud Multiplier, which measures the cost for each dollar of fraud loss, found that this year, every dollar of fraud cost merchants $2.94, up from $2.77 a year ago, a 6-percent increase. The report also found the volume of successful and thwarted fraudulent attempts rising steeply at the companies surveyed — from a monthly average of 238 to 306 successful fraudulent transactions, year-on-year, and from 257 to 313 prevented fraudulent transactions.

Analysts pointed out that mobile commerce continues to be the sector most susceptible to fraud, particularly identity fraud. Mid- to large-size mobile commerce merchants that sell digital goods see 39 percent of the fraud losses from identity theft, including synthetic identities.

Though these merchants appear to have shown signs of investing in fraud prevention solutions in the past year, LexisNexis Risk Solutions noted that many still struggle with identity fraud. This is likely due to the types of solutions that these merchants are implementing.

“The hotly competitive retail landscape means merchants must meet customer expectations for convenience and continually drive business growth,” said Kimberly Sutherland, senior director, fraud and identity management strategy at LexisNexis Risk Solutions. “However, these key drivers also have increased risk for identity-related fraud, especially with the rise of synthetic identities and the volume of botnet orders.

“Therefore, it’s crucial for retailers to not just invest in a large number of fraud prevention solutions, but the right combination and layering of the solutions to defend against different threats,” Sutherland continued.

“Retailers are beginning to demand solutions that combine physical identity data with digital identity data so that they have 360 degree view to know if the person they are doing business with really is that person,” she went on to say.

Other findings of the report include:

• Digital goods merchants who layer core, identity and fraud transaction solutions have lower fraud costs ($2.88 for every $1 of fraud) than those that use only a limited set of core solutions (up to $3.61 per $1 of fraud).

• The LexisNexis Fraud Multiplier has risen most sharply, year-on-year, among those selling digital goods through the mobile channel. For every $1 of fraud, mid- to large-mobile commerce merchants selling digital goods are hit with an average cost of $3.29, as opposed to their physical goods-only counterparts at $2.78.

“Retailers are more likely to be tracking where they’ve successfully thwarted fraud rather than also tracking where they’ve been able to prevent it from occurring. This approach lessens the overall effectiveness of preventing fraud, given that fraudsters are adept at testing for areas that are less of a focus by merchants, and change their attack points accordingly,” Sutherland added.

This is the ninth annual comprehensive research study on U.S. merchant fraud produced by LexisNexis Risk Solution. The methodology of this study targeted U.S. retailers with a comprehensive survey of 703 risk and fraud executives conducted during March. Respondents represented all channels, company sizes, industry segments and payment methods.

For more information, visit https://risk.lexisnexis.com or https://www.relx.com/.

Criminals are becoming more creative in their approach to commit synthetic ID fraud, and new technology recently detected a ploy by an individual who tried a scheme at two different Michigan dealerships.

According to the Federal Trade Commission, 1.7 percent of identity fraud complaints indicated that an auto-finance contract had been generated fraudulently, up from 0.8 percent in 2015.

To curtail this trend, Equifax is working with Oplogic, a company that manages and processes customer information with a simple ID scan, to help reduce unwanted threats stemming from synthetic ID fraud.

The Synthetic ID fraud occurs when a criminal combines real (usually stolen) and fake information to create a new identity. The two companies’ solutions recently helped stop an auto crime at a Michigan dealership.

Driver’s Synthetic Identity Verification from Oplogic, powered with Equifax identity validation tools, is helping dealers reduce unwanted threats. In the attempted fraud scam, a woman visited a dealership with the intent to purchase a vehicle. When she presented her Texas driver’s license, the dealership concluded that the license was synthetic after running a license scan in the patented Oplogic Deal Operator CRM system.

When the same person made a similar attempt shortly thereafter at a different dealership that uses Oplogic Deal Operator CRM, authorities made an arrest.

“The Oplogic Deal Operator CRM combined with Equifax fraud detection and identity validation tools is helping dealerships stop criminals in their showrooms before the crime occurs,” Oplogic president John Parent said. “This adds a much-needed level of protection for dealers and lenders.”

Using this system, dealers can identify fraudulent credentials early in the sales process and before the test drive occurs. The process involves the dealership scanning the potential buyer’s driver’s license using Oplogic CRM software. During the scan, the license is verified against Equifax data and fraud tools to confirm identity.

“Fraudulent activity has become more complex over the years, and it continues to cost billions in lost revenue for dealers and lenders,” said Ken Allen, senior vice president of identity and fraud at Equifax.

“Our data analytics platforms have also become much more sophisticated, and in partnering with leading solution providers such as Oplogic we are making great strides in reducing the number of fraudsters who attempt to create synthetic identities inside the showroom,” Allen went on to say.

Equifax has expanded its set of offerings that help mitigate synthetic ID fraud with the addition of FraudIQ Synthetic ID Alerts — which are based on patent-pending algorithms that analyze attributes such as authorized user velocity and identity discrepancies to help determine if the identity presented could be synthetic.